Baseline analysis and findings

This chapter of the report presents the results of the baseline analysis, focusing on the most notable findings (note - some percentages sum to greater than 100% due to rounding). This section is structured as follows in order to answer the research questions:

- Current travel behaviours and habits

- Current user perceptions on the usability and accessibility of transport, employment and key services

- Status of the local economy in the Levenmouth area [and Tourism]

- Intentions to use the Levenmouth Rail Link

- Travel behaviours if the Levenmouth Rail Link was not reopened.

Current travel behaviours and habits

This section sets out the baseline travel and transport context for Levenmouth. Secondary datasets from Census 2011 and public transport operators have been used, supplemented by information gathered from the Residential Survey.

Current transport services and network

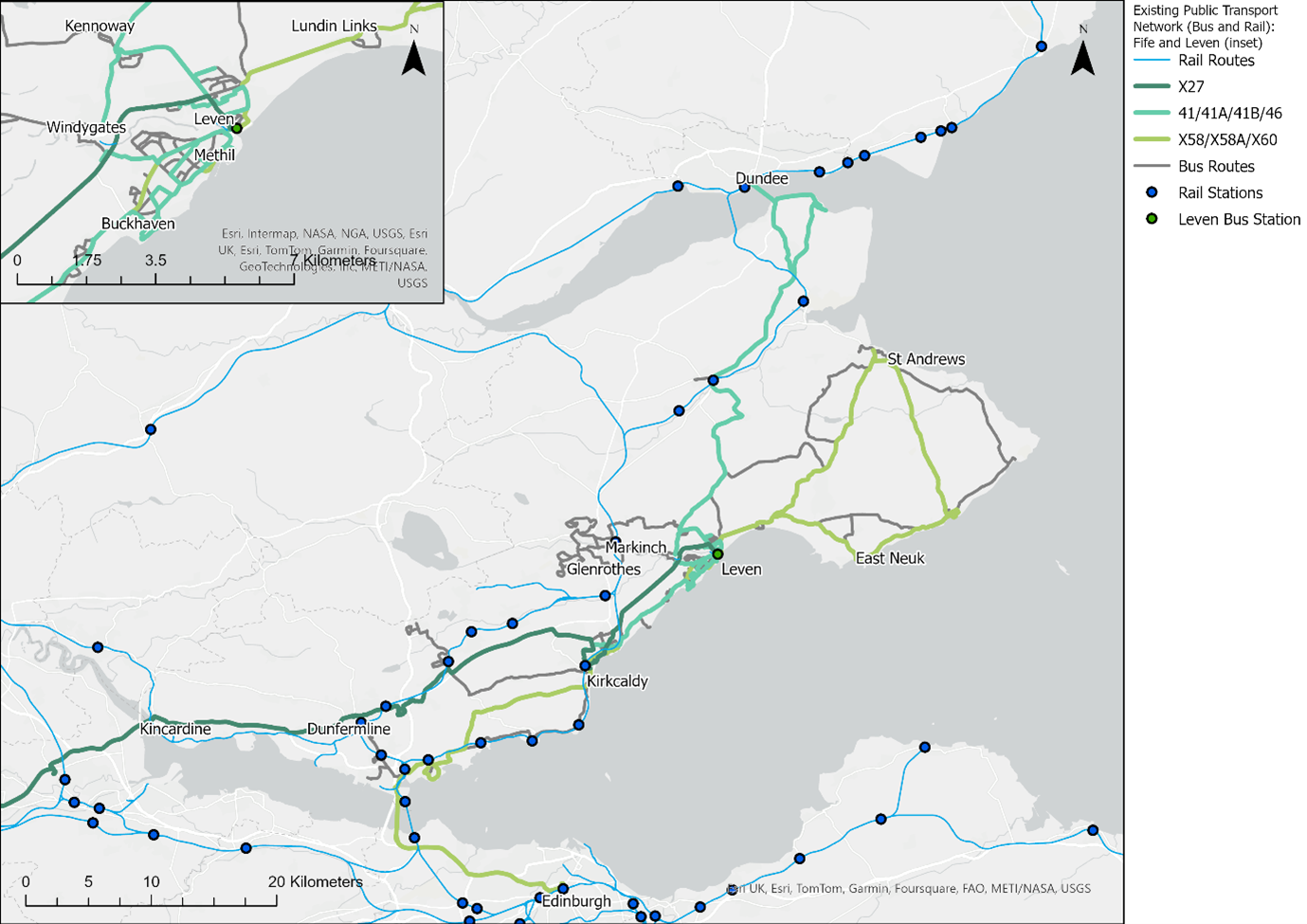

Figure 4‑1 depicts the transport network, as of May 2024, that is available within Levenmouth, Fife and into the neighbouring local authorities. This section provides details on the transport provision that is available to Levenmouth.

Bus

Bus is the main form of public transport provision in Levenmouth. Many of the services operate via Leven Bus Station – located at the south-end of Leven High Street at the A955. Local bus services offer direct connections between the areas within and villages around Levenmouth, to many of the larger settlements in Fife, such as Kirkcaldy, St Andrews and Dunfermline. Direct bus services to the cities of Glasgow, Edinburgh and Dundee are also available from Leven Bus Station. These bus services provide an important link for accessing employment as well as other destinations and trip generators.

Stagecoach East Scotland is the main bus operator in the region and operates the main services connecting Leven to the towns and cities listed above. Some of the main connecting services are:

- X27: Leven – Kirkcaldy – Cowdenbeath – Dunfermline – Glasgow

- X58/X60: Edinburgh – Kirkcaldy – Leven – St Andrews

- 41/41A/41B/46: Kirkcaldy – Leven – Cupar – Dundee

This reliance on bus extends beyond Levenmouth to the East Neuk of Fife (eastern coastal area). This is apparent from the transport network shown in Figure 4‑1, evidently due to there being no rail lines and railway stations present in this area, with the nearest railway station, Markinch Station, located towards Glenrothes.

Journey time modelling undertaken indicated approximately 90% of the Levenmouth population can access the Leven Bus Station within a 20-minute journey by bus or bike; whilst less than 30% of the population can access it by walking. Full results of the modelling can be seen in Appendix C in the accompanying technical appendices.

The ‘Access to Essential Services and Trip Generators’ section reports on the current journey times between Leven and other settlements and cities based on the current public transport network.

Access to the rail network

Figure 4‑1 shows that Leven and the East Neuk of Fife (including villages such as Elie, Anstruther and Crail) are not served directly by the rail network. The closest railway stations to many of these areas, or certainly in the case of Levenmouth, are found to the west with Markinch, Glenrothes with Thornton and Kirkcaldy.

There are bus services connecting Levenmouth to the closest railway stations for onward travel, however, the time it takes to travel to those railway stations plus the requirement for interchange may impact potential rail passenger numbers due to it being less attractive compared to the likes of car which be more direct.

- Analysis using TRACC (TRansport ACCessibility) software for journey time accessibility modelling indicated that only 28% of the total Levenmouth population can access the rail network at Markinch railway station within a 30 minute journey time by public transport (bus). Almost nine in ten people (89%) can access the railway station within a 60 minute journey time. See Appendix C in the accompanying technical appendices for further details.

Reliability of public transport

The reliability of public transport to the region is important given the limited number of transport alternatives, outside of car, which are available to residents.

No data was made available on the punctuality and reliability of bus services in the study area. Given that many of the services serving Levenmouth could be categorised as long-distance, it would be more likely that such services would experience delays. Meanwhile local services would be more reliable.

There is data available on the punctuality of rail, whereby each month ScotRail release a performance and reliability score which provides details on ‘the percentage of ScotRail services that arrive or terminate at this location within five minutes of their booked arrival time’. This data is reported for every railway station on the network and also by rail lines as a whole. Reviewing from the 1st of April to the 27th of April in 2024, for railway stations found within proximity to Levenmouth, showed satisfactory levels of performance – note that ScotRail’s’ ‘Moving Annual Average Public Performance Measure (PPM) Target’ is 90.3%. Cowdenbeath Railway Station ranked the highest with 88.4%, Kirkcaldy and Cardenden were on 87.9% and 87.2%, respectively, followed by Glenrothes with Thornton at 82.2%. The notable exception in terms of performance was Markinch Railway Station (the closest railway station to Levenmouth) with a comparatively low score of 67.7%.

The East Suburban Sector (of which the Fife Circle is a part of) achieved a score of 91.8% for the month of April 2024, with a yearly PPM score of 89.3%. Express lines (of which Edinburgh to Aberdeen is a part of) has a yearly PPM of 81.8%.

Travel patterns and demand

Method of travel to place of work or study

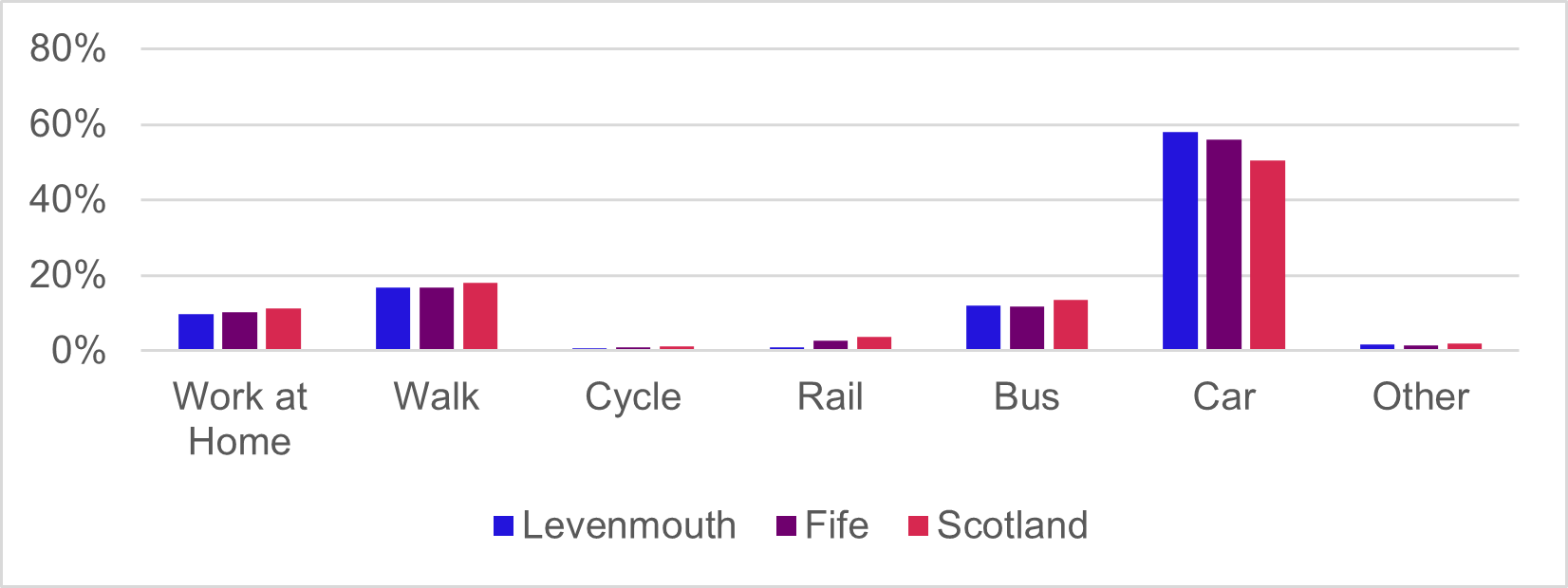

Chart 4‑1 shows the mode share for travel to work or study (Census 2011) as a percentage of the population (all people aged four and over who are studying or aged 16 to 74 in employment in the week before the census).

The dominant and main mode of transport within Levenmouth for travel to work or study is car, which is used by 58% of the population (as defined above). The use of car for such travel is higher in Levenmouth compared to both Fife which is reported at 56% and Scotland at 50%. This shows the reliance on car as a main mode of transport for travelling to ‘work or study’ for people residing in Levenmouth. The second highest mode of transport used for travelling to ‘work or study’ in Levenmouth is walking, with 17%. Walking is likely the preference for more localised travel within Levenmouth itself and is an indication of the number of people living in the settlement area.

Data from the 2011 Census shows that 10% of the Levenmouth population work from home, the same figure as for Fife as a whole and close to the figure for Scotland (11%). It is worth noting the limitations with using 2011 Census data, as this is before the COVID-19 Pandemic in 2020. Since then, hybrid or remote working arrangements have become more common, particularly in certain employment industries that lend themselves to such an arrangement. Analysis undertaken by Scotland’s Census following publication of the 2022 Census mode share results indicates at a Scotland-level, there has been an increase in the proportion home working since the COVID-19 Pandemic (Method of travel to place of work or study | Scotland's Census).

Rail has historically not been used as a means of travel to work or study by the people residing in Levenmouth. Less than 1% of the population use rail as their main mode of transport to ‘work or study’. This is lower compared to the rest of the region, with 3% of the population of Fife using rail, compared with 4% nationally. This indicates existing limited availability of the rail network to residents in Levenmouth, which clearly impacts on the number of people choosing rail as a main mode of transport.

The 2011 Census mode share (based on all people aged four and over who are studying or aged 16 to 74 in employment in the week before the census) has been compared to the residents’ survey completed for this baseline evaluation study. Whilst the results are not directly comparable, it could give an indication as to the change in mode share since the 2011 Census:

- A much higher percentage of survey respondents (living in Levenmouth) indicated they drive to work (86% vs 58%)

- A smaller percentage of respondents living in Levenmouth indicated they walked to work (4% vs 17%); and took the bus to work (4% vs 11%)

- A much lower percentage of respondents living in Levenmouth indicated they work from home now (1% vs 10%). Note – this is not consistent with analysis from Scotland’s Census 2022 which indicates that at a national-level, the working from home mode share has increased.

Car and van availability

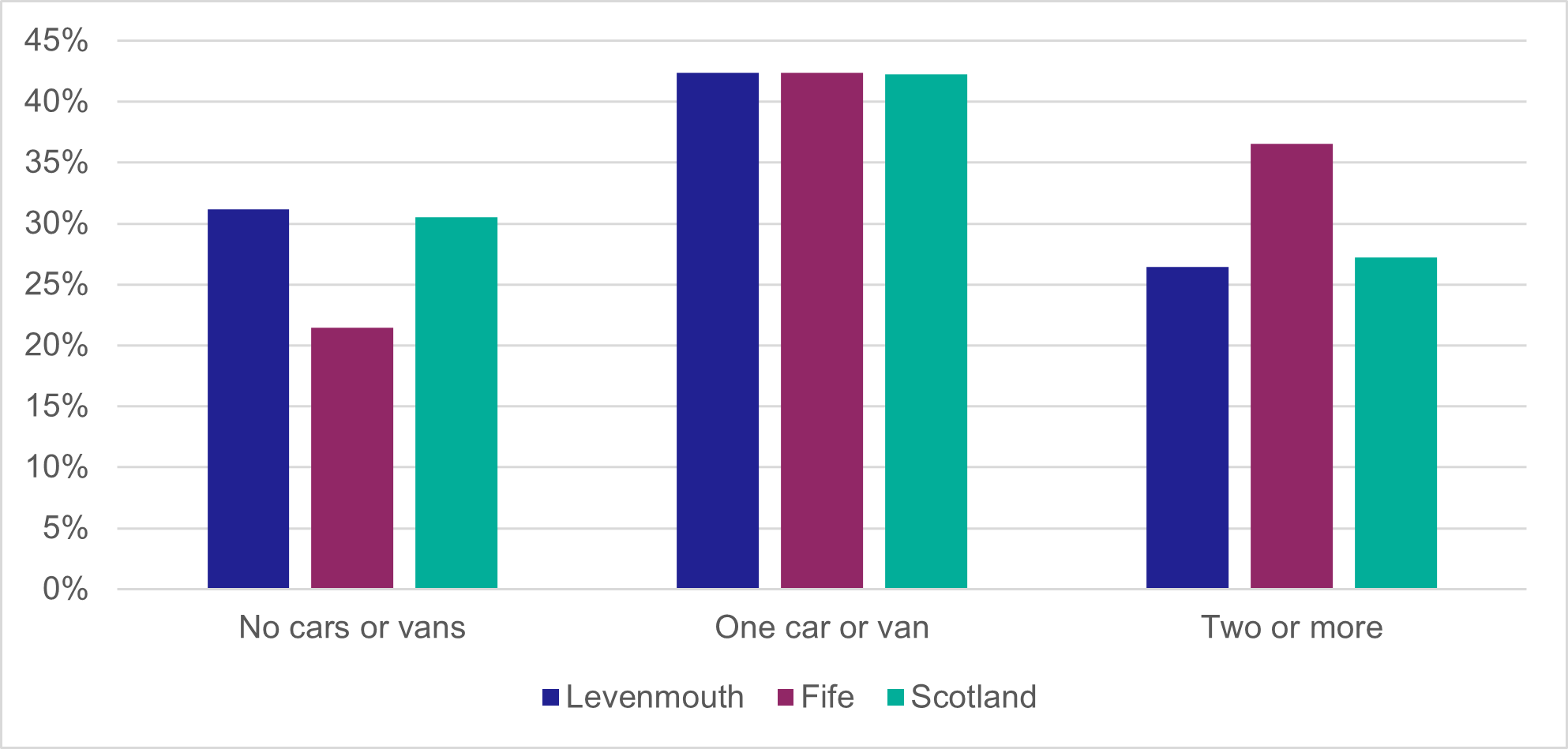

Census data shows that a higher proportion of households in Levenmouth do not own or have access to a car or van for private use, when compared to Fife as a whole: 31% and 21% respectively. The figure for Levenmouth is in line with Scotland, as shown in Chart 4‑2. This proportion of the households will likely be more reliant on public transport for access to services and employment. The percentage of households who own or have access to one car was the same across Levenmouth, Fife and Scotland (42%). Furthermore, only 26% of households in Levenmouth has access to two or more cars or vans, compared with 37% for Fife and 27% for Scotland.

As seen in the section above, just over half of the population (all people aged four and over who are studying or aged 16 to 74 in employment in the week before the census) of Levenmouth (58%) use car as their main mode of transport to work or study. However, 31% of households in Levenmouth do not own or have access to a car or van. This indicates that the population who do own or have access to a car are particularly reliant on this mode of travel.

These Census figures have been compared to the residents’ survey, whereby:

- A much higher percentage of households (80%) in the survey have at least one or more cars that was either owned or available for use by members of their household. Most commonly, this was a single car (39% of respondents) or two cars (35% of respondents).

- Within Levenmouth, Methil respondents had the lowest percentage of households without access to a car (33%), whilst Buckhaven had the highest (89%) percentage of respondents indicating they had no access to a car.

Traffic count data

Figure 4‑2 shows the average traffic count over a 5-day period (Monday – Friday) in 2023.

A trend in the traffic flows travelling south down the A915 can be noted that after the junction with Glenlyon Road and Kennoway Road. The average traffic flows on the A915 corridor increases from 9,400 before the Glenlyon Road and Kennoway Road junction to 15,600 (an increase of 6,200 in vehicles). This suggests there is a notable road user demand travelling south from Levenmouth, which may be linked to accessing employment and key destinations found to the south of Fife, such as in Kirkcaldy and Dunfermline, as well as Central Belt (Edinburgh and Glasgow).

The reopening of the Levenmouth Rail Link may result in a change of mode share and particularly from car to rail within the surrounding area. The better access to rail and reduction in journey time for travelling to cities and key settlements will make rail more competitive compared to car and a more attractive option for travel. Currently car is the dominant method of travel to employment and likely other destinations, as already indicated in this chapter.

Rail network demand

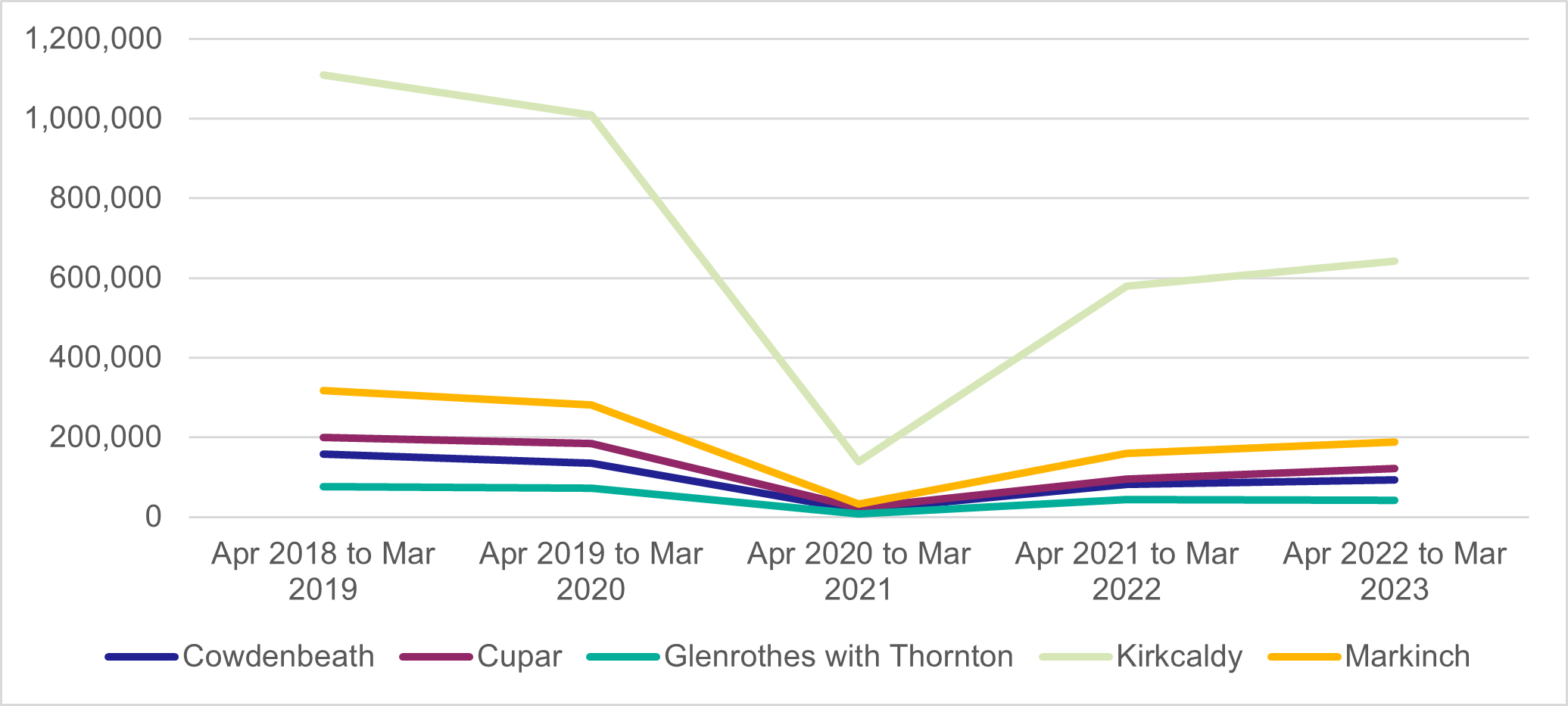

Data provided by ScotRail reported the number of passenger entries and exits for each railway station from 2018/19 to 2022/23. Chart 4‑3 shows the patronage demand for five railway stations found in close proximity to Levenmouth. All railway stations follow a similar trend, whereby patronage dropped in 2020/21 as a result of the travel restrictions put in place during the COVID-19 pandemic. Patronage then subsequently increased in 2021/22 and 2022/23 as travel restrictions were lifted.

The 2022/23 figures for the five railway stations are between 55% and 61% of 2018/19. Cupar saw 61% passenger numbers in 2022/23 when compared with 2018/19. Cowdenbeath, Kirkcaldy and Markinch were at 60%, 58% and 59% respectively. Glenrothes with Thornton was the lowest with 55% of the passenger numbers recorded in 2018/19.

Across the Fife railway stations passenger entry and exit numbers were just over six million in 2018/19. The figure for 2022/23 was substantially lower at just over three and a half million which represents a 41% decline over the 5-year period. However, passenger numbers are on an upward trend as in 2021/22 there were just under three million passengers. The increase from 2021/22 to 2022/23 was 20%.

Rail passenger numbers

The LENNON (Latest Earnings Networked Nationally Over Night) system holds information on the vast majority of national rail tickets purchased in Great Britain and is used to allocate the revenue from ticket sales between train operators. It therefore provides information on patronage rail journeys to and from stations. The three railway stations in closest proximity to the Levenmouth Rail Link – Markinch, Kirkcaldy and Glenrothes with Thornton – will be used to understand the rail travel patterns and movements originating from the area.

| Origin Railway Station | Total Passengers from Origin | Fife | Edinburgh | Dundee | Aberdeen | Other |

|---|---|---|---|---|---|---|

| Cowdenbeath | 90,000 | 18% | 68% | 1% | 0% | 12% |

| Cupar | 120,000 | 20% | 44% | 18% | 3% | 16% |

| Glenrothes with Thornton | 38,000 | 21% | 65% | 0% | 0% | 14% |

| Kirkcaldy | 476,000 | 16% | 56% | 5% | 1% | 22% |

| Markinch | 204,000 | 15% | 54% | 7% | 2% | 22% |

The LENNON data in Table 4‑1 shows the majority of rail trips originating from these stations in 2023/24 travelled to other railway stations within Fife or to Edinburgh (comprising Waverley and Haymarket). Edinburgh was the main destination for people travelling from the three closest stations to Levenmouth – accounting for a minimum of 54% of outbound trips (Markinch – 54%, Kirkcaldy – 56%, and Glenrothes with Thornton – 65%).

As expected, all railway stations showed a drop in passenger numbers during the COVID-19 pandemic as a result of travel restrictions put in place, and patronage demand has remained relatively low compared to pre COVID-19 levels. The following bullets provide a summary for each station. Note – the annual numbers quoted are based on April to March (I.e. 2023/24 refers to April 2023 to March 2024):

- Kirkcaldy Railway Station:

- This railway station has the highest patronage of all the stations in close proximity to Levenmouth, with a total of 476,000 originating passengers recorded for the year 2023/24. This is a 38% reduction (approximately 290,000 less passengers) compared to 2018/19 (pre-COVID-19 levels).

- Between the years 2022/23 and 2023/24, there was an 18% increase in patronage at Kirkcaldy Railway Station – from approximately 390,000 to 476,000 passengers, respectively.

- In terms of where people are travelling to, from Kirkcaldy Railway Station:

- The majority of trips (56%) are to Edinburgh.

- Up to 16.2% of rail trips are to Fife railway stations.

- Other notable destinations trips are made to from Kirkcaldy Railway Station include to Dundee (5% of all trips) and Aberdeen (0.7% of all trips).

- Markinch Railway Station:

- Reported 204,000 originating passengers for 2023/24, a 22% decrease (drop of 57,000 passengers from 261,000) compared to pre COVID-19 levels for the year 2018/19.

- Patronage numbers for 2023/24 increased by 23% (an increase from 157,000 to 204,000) compared to the year 2022/23.

- In terms of where people are travelling to, from Markinch Station:

- The majority of trips (54.6%) are to Edinburgh; followed by

Fife railway stations, accounting for 14.7% of all trips.

- Other notable destinations included Dundee and Aberdeen which attracted a proportion of rail trips, with 7% and 2.4% of all trips respectively.

- Cupar Railway Station:

- Reported 120,000 originating passengers for the year 2023/24, representing a 13% decrease (drop of 18,000 passengers from 138,000) compared to 2018/19 pre COVID-19 levels.

- Cupar saw the highest originating patronage increase across the five stations, of 31% from 2022/23 to 2023/24 (an increase from 82,000 to 120,000).

- In terms of where people are travelling to, from Markinch Station:

- Up to 44% of trips are to Edinburgh.

- Up to 20% of trips are to Dundee.

- Up to 18% of trips are to railway stations within Fife.

- Up to 3% of trips are to Aberdeen.

- Cowdenbeath Railway Station:

- Reported 90,000 originating passengers for the year 2023/24, representing a 25% decrease (drop of 30,000 passengers from 120,000) compared to 2018/19 pre-COVID-19 levels.

- Patronage levels increase by 24% from 2022/23 to 2023/24 (an increase from 69,000 to 90,000, respectively).

- In terms of where people are travelling to, from Cowdenbeath Station:

- The majority of trips (68%) are to Edinburgh.

- Trips to Dundee and Aberdeen make up 1.2% and 0.2% of trips, respectively.

- Glenrothes with Thornton Railway Station:

- Reported the lowest rail patronage levels of the stations in close proximity to Levenmouth, with 38,000 originating passengers in 2023/24.

- There was a 22% increase in patronage between 2022/23 and 2023/24 (an increase from 30,000 to 38,000, respectively).

- In terms of where people are travelling to, from Glenrothes with Thornton Station:

- The majority of trips (65%) are to Edinburgh; followed by Dundee which accounts for 21.2% of all trips.

The destination figures for each of the railway stations highlighted above, i.e. rail journeys travelling to and destinating at these railway stations, reported much lower levels compared to rail trips originating at these stations.

- Kirkcaldy Railway Station was the destination for 209,000 passengers between April 2023 and March 2024, which is a 56% less than the total number of passengers who used this railway station as an origin.

- Similarly, Markinch Railway Station (58,952 passengers) and Glenrothes with Thornton Railway Station (12,531 passengers) between April 2023 and March 2024 observed notably lower destination patronage compared to origin trips.

This would suggest that not all trips from these railway stations are return journeys (e.g. such as a return trip during the day for commuting) and therefore people are travelling for a range of purposes.

Impacts on rail travel in Scotland

Impact of COVID-19

Scotland’s rail system faced significant challenges during the COVID-19 pandemic. It led to an unprecedented decline to rail patronage levels across the country, as a result of travel restrictions put in place and resulting in the level of service being reduced during this period. The number of annual passengers using rail services between April 2020 and March 2021 had dropped by as much as 85% across Scotland compared levels before the pandemic between April 2018 and March 2019 – 194 million to 30 million annual passengers. This decrease in annual passengers comparing the same periods was slightly higher in Fife, with patronage levels on average down by 89% during the pandemic compared to pre COVID-19 levels. This was similar for the railway stations found in close proximity to Leven, with Markinch and Glenrothes with Thornton reporting a decrease of 90%.

There are lasting impacts from the pandemic which have led to a change travel behaviour and patterns across the country, with more people choosing hybrid or remote working who work within industries that permit such an arrangement. There is a greater acceptance from employers to provide more flexibility working.

The data presented in Section 4.1 indicates that rail use is gradually recovering and increasing towards levels before the pandemic, however, it is currently uncertain whether rail use will return to levels observed before pandemic in the near future.

Impact of Peak Fares Removal Pilot

The ‘ScotRail Peak Fares Removal Pilot’ was initiated by the Scottish Government in as part of their efforts to encourage public transport use and assess the impact on passenger behaviour and the rail network. The pilot aimed to encourage modal shift from private car to rail while making rail travel more affordable and accessible over the pilot period.

The final evaluation report covers the period from its introduction in October 2023 to the beginning of July 2024 and provides insights into the outcomes of the pilot. The report suggests that the pilot has been successful in improving awareness of rail as a viable travel choice and that it significantly reduced the cost of travel by rail at peak times. The analysis showed that there was a limited increase in the number of passengers during the pilot, it did not achieve its aims of encouraging a significant modal shift from car to rail. The report concluded that the pilot primarily benefitted existing train passengers and those with medium to higher incomes. Although passenger levels increased to a maximum of around 6.8%, this was not enough to make the policy self financing.

Impact of new rail infrastructure

The Borders Railway is the most recent new rail line to have been constructed and opened in Scotland. Evaluation and monitoring studies have been carried out to understand the impact of the scheme and whether the objectives set out have been achieved. The conclusions of those studies, covering the impacts within the study area on travel behaviour and demand, living choices and the economy, is summarised below.

The Borders Railway, which connects Edinburgh with the Scottish Borders (with railway stations in Stow, Galashiels and Tweedbank), opened in 2015. Subsequent evaluations of the new rail line, which has involved on-train surveys, telephone surveys to capture infrequent users of the service, and secondary data analysis using data such as ticket sales, concluded the following:

- There was evidence to suggest that the railway has enabled new journeys to be made that were not possible prior, with around a third of respondents stating they did not make their current trip previously.

- Results suggested a notable modal shift for journeys, with around two thirds of respondents now using another mode, and particularly from car to rail with two thirds of those respondents stating they previously drove all the way to their destination. There was also evidence of modal shift from bus to rail.

- The railway has impacted on people’s residential choice, with evidence to show that people have consciously moved to the area as a result of the rail reopening. Of the respondents who had moved to the area following the opening of the new railway, well over half had stated that the new rail line was a major factor in moving to area.

- The Year 2 Evaluation results suggest that the railway has resulted in some changes to car ownership levels. Six per cent of survey respondents indicated that since the opening of the Borders Railway, they have reduced the number of vehicles in their household as a result of taking the train for journeys they previously took by car; whilst 1% of respondents had increased the number of vehicles in their household to allow them to drive to the new stations (and a further 1% increasing the number of vehicles at their household due to removal/changes to bus routes).

- There is evidence that the railway had a material impact on leisure and tourism travel in the corridor, both to and from Midlothian and the Scottish Borders, with the railway being identified as a key driver for this activity.

While there are several factors that can impact the use and performance of a new rail line, there are some similar characteristics comparing Levenmouth Rail Link to The Borders Railway which assist in identifying areas that may be impacted. Both rail lines are situated in a rural setting and offer a connection to Edinburgh, where employment opportunities and other key destinations are found. Furthermore, both rail services offer an hourly frequency and have comparable journey times travelling to Edinburgh which can be reached in just over an hour (Waverley Railway Station to Tweedbank Railway Station and Leven Railway Station). However, it should be acknowledged that The Borders Railway is significantly larger in scale and is one of the longest stretches of railway to be reopened in the UK over the past century. The Borders Railway has a rail track length of around 50km compared to 8km for Levenmouth Rail Link. The Borders Railway is an entirely new rail line serving a key southern corridor through the Borders and connects several settlements found along the line to Edinburgh City, whereas Levenmouth Rail Link directly connects the Levenmouth area to the existing rail network.

Household travel arrangements and personal travel habits

Resident survey response rates and analysis note

This section provides several of the results from the residents primary data collection undertaken as part of this study. The results are reported initially at the overall sample level, followed by more area specific results (i.e. areas within Levenmouth). The percentages provided against results from these specific locations are based on a lower number of respondents at these areas and therefore may not be representative of the entirety of these areas. The smaller area samples may affect the generalisation of the findings within those areas and should be taken into consideration when interpreting the results. Due to the small sample sizes for specific geographic areas, caution should be taken when interpreting percentages. In Section 2.2, Table 2‑1 provides the actual number of respondents from each area, giving an indication of what the percentage results represent in the analysis below. Throughout the analysis below, respondent and resident are used interchangeably. Note – no detailed tests have been carried out determine ‘statistical’ significance, As no significance testing has been undertaken, this means any differences between groups of respondents could have occurred by chance due to sampling variation, rather than being a true difference in the population, especially where an apparent difference is small.

Frequency of travel by mode

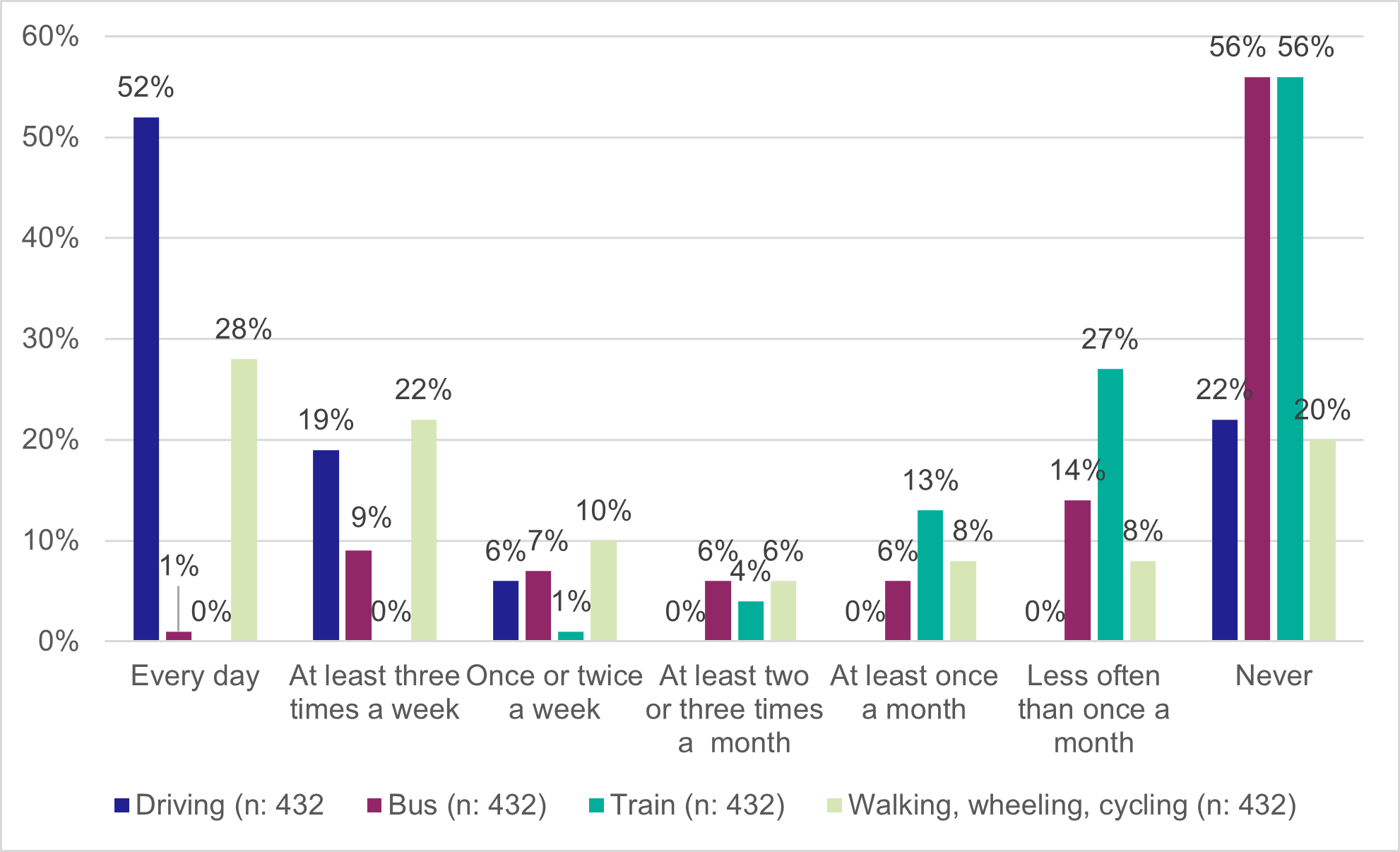

This section outlines personal travel habits and household arrangements by mode, with Chart 4‑4 below showing the frequency each mode is used. This is then summarised in the subsequent paragraphs.

Car ownership and usage

The majority of households (80%) had at least one or more cars that was either owned or available for use by members of their household. Most commonly, this was a single car (39% of respondent households) or two cars (35% of respondent households). Within Levenmouth, up to 77% of households have access to one or more cars. Methil had the highest percentage of households without access to a car (33%) whilst Buckhaven has the highest percentage of households with access to one or more cars (89%).

Analysis of the full sample of respondents indicate that 52% drive a car or van for private purposes each day (including travel to work but not travel as part of their job) with a further 19% indicating that they do so at least three times per week. Up to 22% of respondents indicate that they never drive a car/van for private purposes.

Across the respondents from Levenmouth, 52% indicated they also drive a car of van for private purposes each day (including travel to work but not travel as part of their job). Each of the settlements within Levenmouth display similar results, though of the various sub-sample analysis of these areas in Levenmouth, 60% of Buckhaven residents drive a car or van for private purposes every day, whilst 32% of Methil residents do not drive a car or van every day for private purposes.

Bus usage and concessionary cards

The analysis of responses of the whole study area indicates that over half of the residents say they never use the bus (56%) and among those that do use the bus this is most commonly at least two or three times a month or less often (26%). A further 17% of residents say they use the bus once or twice a week or more often.

For Levenmouth (i.e. Leven, Methil, Buckhaven and Kennoway), 64% of residents never use the bus; and only 1% of Levenmouth residents use the once every day. Only 3% of Kennoway and Buckhaven, and 1% of Methil residents use the bus every day; whilst the greatest percentage of residents using the bus at a higher frequency, for at least three times a week was found in Methil (10%). The following percentage of residents within areas of Levenmouth never use the bus: Buckhaven (69%), Leven (67%) Kennoway (52%) and Methil (52%).

Of those that were able to provide information on the number of concessionary cards held by people in their households that enable them to travel free on local bus services, the average number of cards held was 0.90 cards per household, these most commonly being Over 60 Cards (0.49 cards per household) and Young Persons’ (Under 22) Cards (0.35 cards per household).

Rail usage

The majority of residents say they never use the train (56%) and among those that do use the train this is most commonly at least two or three times a month or less often (44%). A further 1% of residents say they use the train once or twice a week or more often.

Up to 74% of Levenmouth residents indicated they do not use the train; and no Levenmouth respondents indicated they used the train every day. Amongst the settlements within Levenmouth (i.e. Leven, Methil, Buckhaven and Kennoway), between 71% and 77% of those residents do not use the train for any journeys. It is notable however only 40% of residents within other areas within Levenmouth (such as Lundin Links, Largo Ward to the east and the Wemyss Villages to the west) indicated they never use the train.

Of those residents within Levenmouth who do use the train:

- approximately 20% use it less often than once a month (with Kennoway having the highest percentage (29%) of residents traveling this frequently by train.

- Approximately 5% travel at least once a month by train (with Buckhaven having the highest percentage (9%) of residents travelling this frequently).

By comparison:

- Glenrothes and Kirkcaldy which do have their own railway stations:

- Similarly low number of residents who use the train more frequently (every day to once or twice a week) compared to Levenmouth residents, however over duration of a month there is a greater propensity to use the train for journeys, whereby:

- approximately 4% of Glenrothes and 15% of Kirkcaldy residents use the train at least three times a month; and

- 30% of Glenrothes and 39% of Kirkcaldy residents use the train at least once a month.

- At least 54% of Glenrothes and 41% of Kirkcaldy residents use the train less often than once a month.

- Similarly low number of residents who use the train more frequently (every day to once or twice a week) compared to Levenmouth residents, however over duration of a month there is a greater propensity to use the train for journeys, whereby:

- Cupar, which also has a railway station within the town, is however more comparative in terms of resident usage with Levenmouth.

- East Neuk residents have a slightly higher propensity to use rail services compared to Levenmouth, whereby 3% indicate they travel by train at least once or twice a week (compared to 0%) and 10% at least three times a month (compared to 1%). Only 60% of East Neuk residents never travel by train, compared to 74% of Levenmouth residents.

Walk, wheel or cycle

The majority of all respondents say they frequently walk, wheel or cycle for everyday journeys (for example, travel to work, education, shops or healthcare) with 60% doing so once or twice a week or more often. A further 22% walk, wheel or cycle at least two or three times a month or more often and the remaining 20% never walk, wheel or cycle.

Notable results from the Levenmouth areas include:

- The majority (94%) of Kennoway residents walk, wheel or cycle at least once or twice a week or more (compared to a 49% Levenmouth average), with 39% walking, wheeling or cycling for everyday journeys;

- More than a fifth (23%) of Buckhaven residents walk, wheel or cycle at least once a week for journeys, however a much smaller percentage (12%) walk, wheel or cycle once to at least three times a week compared to the Levenmouth average (29%).

- A greater percentage of the residents in Glenrothes and Kirkcaldy walk, wheel or cycle for everyday journeys (43% and 51%, respectively) compared to the Levenmouth average (20%); with as many as 92% of Kirkcaldy residents walking, wheeling or cycling at least once a week or more.

Employment and education

Two-thirds of survey respondents (66%) were either employed full time, employed part-time or were self-employed. A further 1% were students.

Amongst those respondents that were employed or studying, 30% had their main place of work/study within the Levenmouth area, 62% elsewhere in Fife, 7% in Edinburgh and 1% elsewhere in Scotland.

The majority of these respondents (87%) indicated their usual main method of travel to work/study was by car/van as driver, 2% by car/van as passenger, 5% by walking and 2% by ordinary service bus. Fewer than 1% of respondents (one single respondent) indicated that their usual method of travel to work/education was by rail.

In considering the responses from settlements within the study area:

- Kennoway has the highest percentage of Levenmouth residents (94%) whose main method of travel to work/study was by car, however with the remaining residents (6%) walk;

- The main travel to work/study for the majority of Buckhaven residents (92%) was also by car, with the remaining residents taking either the bus (4%) or working from home (4%).

- Methil residents had the lowest share of car/van drivers (81%), along with the highest sustainable travel mode share with walking (9%) and ordinary bus (7%) as their main method of travel to work/study.

- Up to 8% of residents from other Levenmouth areas (i.e. Largo, Lundin Links, Wemyss Towns) travel as a car/van passenger to work.

- By comparison, Kirkcaldy, Glenrothes and Cupar residents had a similar percentage range of people driving to work/study (between 71% and 94%), as well as travel to work/study by bus (3% to 7%).

- In terms of travel by train to work:

- Only residents living in other areas of Levenmouth (i.e. Lundin Links, Largo, Wemyss Villages) travel by rail to work/study. Given these locations do not have their own railway stations, it suggests that these are actually multi-modal journeys where they either drive, are a passenger, or take the bus to/from the train station.

- None of the residents from areas with railway stations (Glenrothes, Kirkcaldy and Cupar) indicated they travelled by rail to work or education. This is somewhat consistent with the 2011 Scotland Census where rail represented less than 3% of the travel to work/study mode share; and the 2021 Travel and Transport in Scotland where the rail mode share for Fife was approximately 1% (results not disaggregated to settlement level).

Amongst respondents from the whole study area, the median journey time to work/education was in the 10 to 20 minute range with the most common response being in the 20 to 30 minute range. Based on the mid-point of the various bands presented to respondents, the estimated average journey time to work/education is approximately 22 minutes.

Note: The resident survey intended to include the following response categories: fewer than five minutes, between five minutes and ten minutes, between ten minutes and 20 minutes, between 20 minutes and 30 minutes, between 30 minutes and one hour, between one hour and two hours, between two hours and three hours, more than three hours. However, ‘between 30 minutes and one hour’ was omitted from the survey response options. Interviewers included any responses between 30 minutes and one hour within the ‘one hour and two hours’ category. This has been accounted for in the estimated average journey time calculation.

The median and modal number of return trips for work or education per week is five and the average number of return trips is approximately 5.7.

In terms of frequency of return trips to/from work/study, in a typical week:

- Approximately half of Levenmouth residents make five return trips.

- Leven has had the lowest percentage of residents making this number of journeys (35%) whilst Methil had the second highest (58%) and other Levenmouth areas (such as Largo, Lundin Links and Wemyss Villages) has the highest percentage (65%).

- Almost all (97%) of Kirkcaldy residents make five return trips (compared to 65% of Glenrothes residents)

- Between 6% and 12% of Levenmouth residents travel to work/study up to three times a week.

Travel for shopping, leisure and healthcare

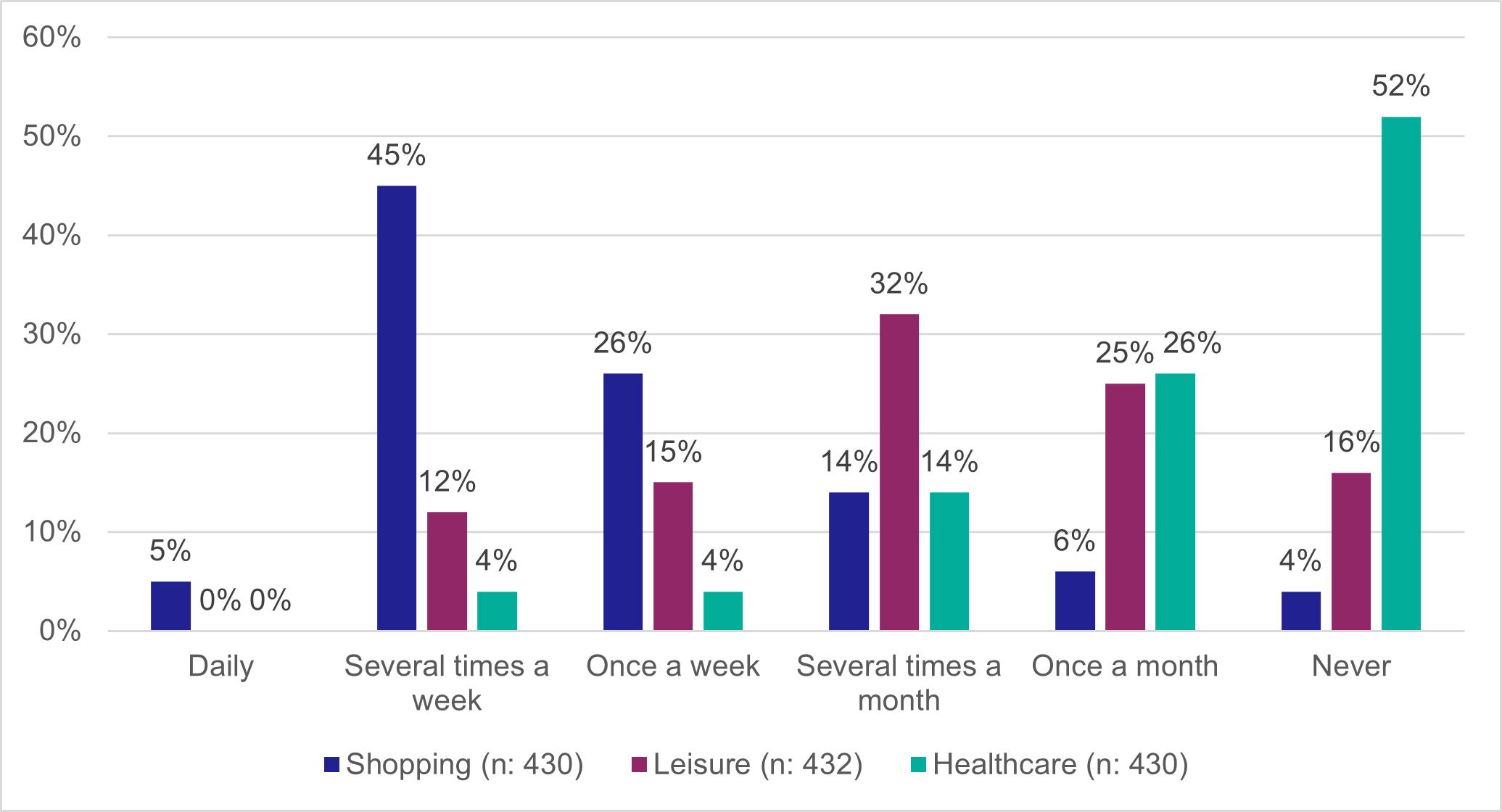

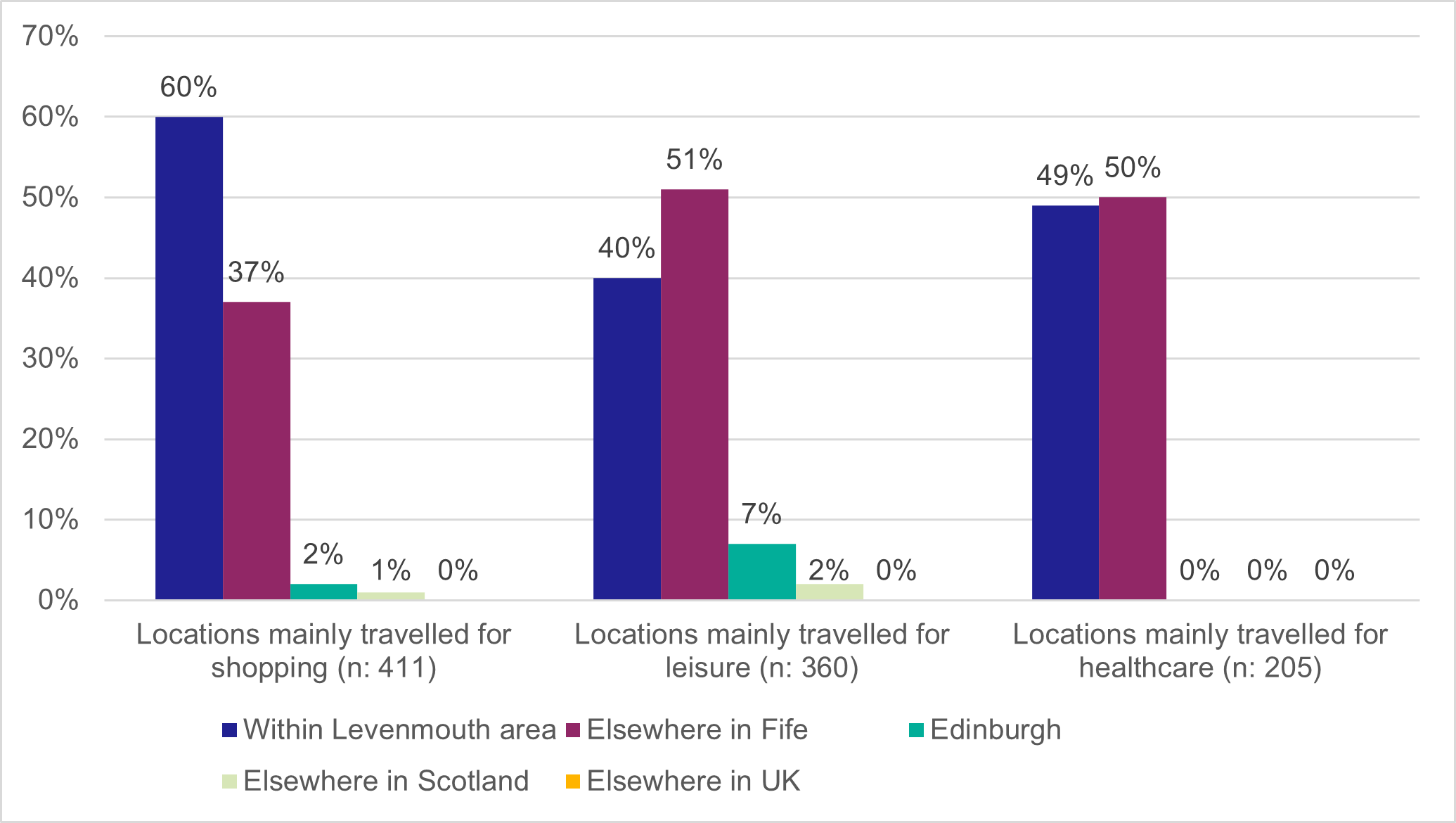

Chart 4‑5 below shows the typical number trips for shopping, leisure and healthcare per month, and Chart 4‑6 shows the locations mainly travelled to for these journey purposes. The data is then expanded in the subsequent paragraphs.

Shopping

Respondents from the whole study are indicate that they travel for the purposes of shopping at the following frequencies: several times per week (45%), once a week (26%) or several times a month (14%). Up to 60% of respondents mainly travel within the Levenmouth area for shopping, 37% elsewhere in Fife, 2% to Edinburgh and 1% elsewhere in Scotland. In terms of respondents from Levenmouth:

- The majority (83%) predominantly do their shopping within Levenmouth, with 14% going elsewhere in Fife for shopping.

- Methil has the highest percentage of residents that mainly shop within Levenmouth (91%), whilst Buckhaven has the lowest percentage of residents who mainly shop in Levenmouth (73%) whereby as many as 21% shop elsewhere in Fife.

When travelling for shopping within Levenmouth (from all survey areas), the most common method of travel is by car/van (either as a driver (63%) or as a passenger (7%), with 1% traveling by car/van using park and ride. Up to 14% indicated that their main method of travel is walking, 13% use an ordinary service bus and 2% travel by taxi/mini cab.

The vast majority of journeys for reasons of shopping elsewhere in Fife are made by car/van (95% total). For residents only within Levenmouth, the highest share of travel by car/van to shopping was found in Buckhaven, where 79% of residents drive for shopping journeys. The lowest was found in Methil whereby 58% of residents drive, but also had the highest percentage of people walking to the shops (22%). Kennoway had the highest share of residents who take the bus to the shops (19%).

Of the seven respondents from Levenmouth who mentioned that they travel to Edinburgh for shopping, five travel by car/van and two travel by rail.

Leisure

Respondents as a whole indicate that they travel for the purposes of leisure several times per month (32%), once a month (25%), once a week (25%) or several times a week (12%), with 16% of respondents indicating that they never travel for leisure purposes. Up to 40% of respondents mainly travel within the Levenmouth area for leisure purposes, 51% elsewhere in Fife, 7% to Edinburgh and 2% elsewhere in Scotland.

For Levenmouth respondents, 55% mainly stay within Levenmouth, 38% travel elsewhere in Fife, 5% to Edinburgh and 1% elsewhere in Scotland. When travelling for leisure within Levenmouth, the most common method of travel is car/van (52% total) – 44% as driver, 7% as passenger and 1% using park and ride. Up to 41% indicate that their main method of travel is walking, 5% ordinary service bus and 2% taxi/mini cab. The vast majority of journeys for reasons of shopping elsewhere in Fife are by car/van (94% total).

For residents living within Levenmouth itself, when travelling for leisure within Levenmouth:

- From Leven, 69% walk, 19% use car/van and 3% use the bus.

- From Methil, 15% walk, 70% use car/van and 9% use the bus.

- From Buckhaven, 58% walk and 42% use car/van.

- From Kennoway, 56% walk and 31% use car/van.

- From other areas within Levenmouth, 25% walk, 43% use car/van and 11% use the bus.

For Levenmouth residents travelling outwith Levenmouth for leisure:

- The majority (80%) travel by car, 4% by bus and 5% by rail to leisure elsewhere in Fife.

- Of the 12 Levenmouth residents who responded on their travel mode to Edinburgh for leisure, 67% of them travelled by car (as the driver), 25% by rail (including P&R) and 8% as a car/van passenger. No respondents indicated they travelled by bus to Edinburgh for leisure.

Healthcare

Respondents indicate that they travel for the purposes of healthcare once a month (26%), several times a month (14%), once a week (4%) or several times a week (4%). Up to 52% of respondents indicate that they never travel for purposes of healthcare. Up to 49% of respondents mainly travel within the Levenmouth area for healthcare purposes and 50% elsewhere in Fife.

When travelling for healthcare purposes within Levenmouth, the most common method of travel is car/van (62% total) - 46% as driver, 15% as passenger and 1% using park and ride. Up to 27% indicate that their main method of travel is walking, 13% use an ordinary service bus and 2% travel by taxi/mini cab. The vast majority of journeys for reasons of shopping elsewhere in Fife are by car/van (92% total).

Within Levenmouth, only 29% of residents from Leven indicated they drive to healthcare (with 39% walking), whilst as many as 68% of Methil and 63% of Buckhaven residents indicated they also drive. Up to 46% of Kennoway residents indicated they walk to healthcare services. The vast majority of journeys for healthcare purposes elsewhere in Fife are by car/van (82% total).

Current user perceptions on the usability and accessibility of transport, employment and key services

This section outlines satisfaction with, and perceptions of, the usability and accessibility of transport employment and key services by users.

It utilises primary data from the Personal Travel Barriers section of the residents’ survey, supported by journey time accessibility modelling analysis which gives an indication of the percentage of residents who can access key services within a given journey time by public transport.

Satisfaction with services

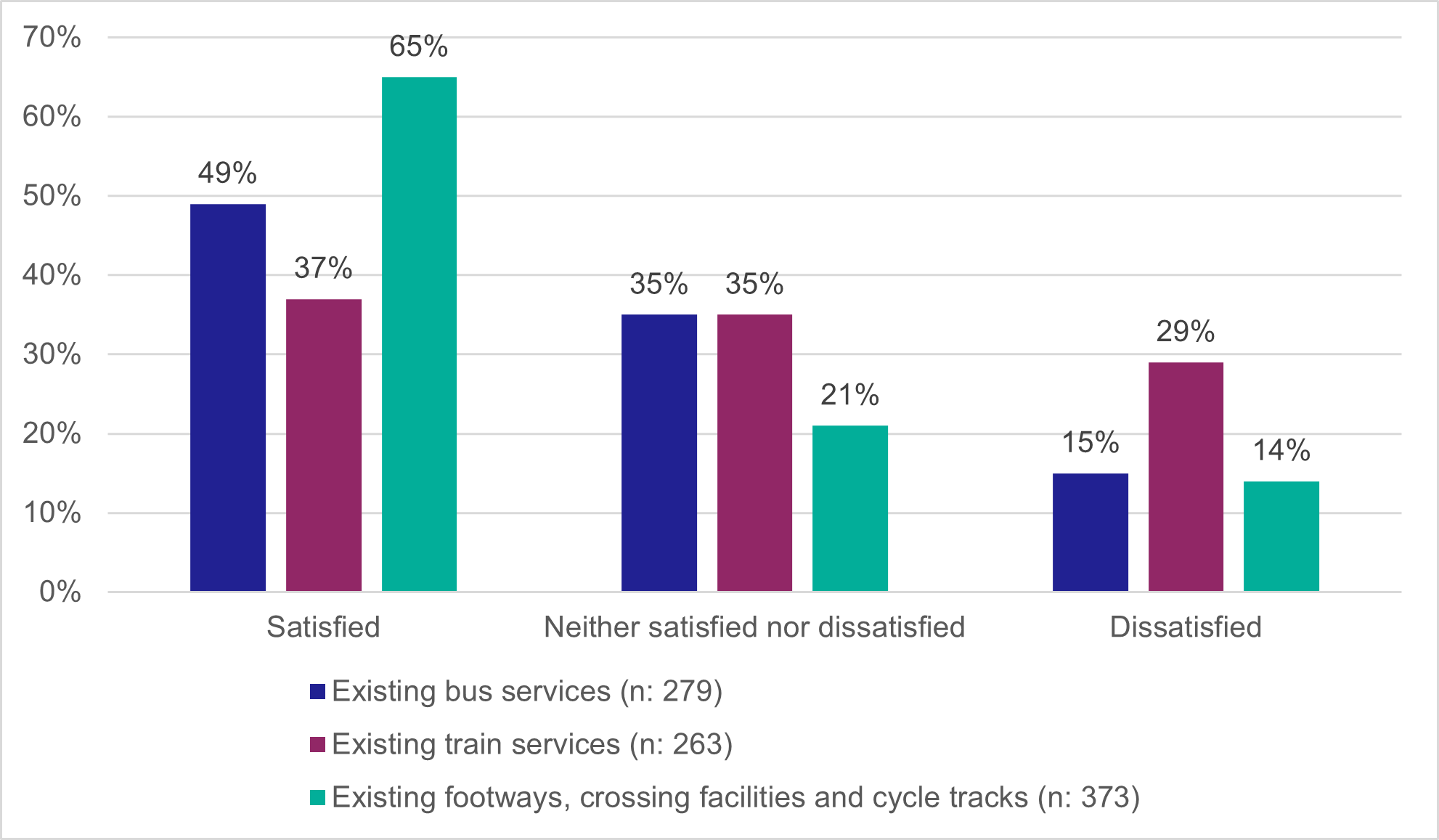

Residents were asked about how satisfied they are with bus and rail services, as well as existing footways, crossing facilities and cycle tracks. The results are shown in Chart 4‑7.

Satisfaction with bus services

Nearly half (49%) of residents that felt they were satisfied with existing bus services while a further 35% were neither satisfied nor dissatisfied. By comparison, 15% of residents were dissatisfied with existing bus services.

Amongst those expressing satisfaction with bus services, the most common factors influencing satisfaction were availability of bus services (34%), accessibility of bus stop and/or bus (32%) and reliability of bus services (28%).

Amongst those expressing dissatisfaction with bus services, the most common influencing factors were frequency of bus services (50%), availability of bus services (48%), directness of bus services (48%) and reliability of bus services (48%).

Satisfaction with rail services

A little over a third (37%) of respondents were satisfied train services, with 29% dissatisfied and 35% were neither satisfied nor dissatisfied.

Amongst those expressing satisfaction with train services, the most common influencing factors were availability of train services (30%), convenience of train services (26%), accessibility of train station and/or train (25%) and reliability of train services (24%).

Amongst those expressing dissatisfaction with train services, the most common influencing factors were cost of train services (44%), frequency of train services (33%), reliability of train services (29%) and availability of train services (28%).

Satisfaction with existing footways, crossing facilities and cycle tracks for walking, wheeling and cycling

A majority of residents that felt they could provide an answer were satisfied with existing footways, crossing facilities and cycle tracks (65%) while a further 21% were neither satisfied nor dissatisfied. By comparison, 14% of residents were dissatisfied with existing footways, crossing facilities and cycle tracks.

Amongst those expressing satisfaction, the most common influencing factors were safety (63%) and availability (also 63%) of footways/crossing facilities/cycle tracks.

Amongst those that expressed dissatisfaction, a notable proportion cited each of safety (85%), attractiveness (79%) and availability (77%) of footways/crossing facilities/cycle tracks as influencing factors on their views.

Personal travel barriers and perceptions of safety

The vast majority of all respondents indicated that they find it quite easy or very easy to access each the following services: education (98%), shopping (93%), employment (92%) and healthcare (90%). Of respondents from settlements within Levenmouth, those that found any difficulties were for:

- Access to shopping (Leven, 3%) – reasons included being availability of public transport, personal circumstances (such as family or childcare responsibilities) and distance to travel;

- Access to leisure (Leven 7%, Methil 1%, Buckhaven 6%) – reasons included availability of public transport, accessibility of public transport, availability of a car, cost of using a car, feeling of safety in getting to places and distance to travel.

- Access to healthcare (Leven, 2%) – the main reason cited was personal circumstances.

Almost two thirds (63%) of Levenmouth respondents say that they feel ‘very safe’ while walking/wheeling alone in their neighbourhood after dark whilst 36% say that they feel ‘fairly safe.’ As many as 79% and 78% of Buckhaven and Leven residents, respectively, feel ‘very safe’, in comparison to only 35% in Kennoway who felt ‘very safe.’ Conversely, 6% of Kennoway respondents indicated they feel ‘fairly unsafe’, compared to 1% of Leven and Methil respondents, each, who feel ‘fairly unsafe’.

Access to essential services and trip generators

Access to employment

The ‘Economic Landscape’ in section 4.3 ‘Status of the local economy in Levenmouth’ reports that there are over 9,000 jobs found within Levenmouth area. The majority of these jobs are categorised within the following industries: ‘Mining, Manufacturing & Utilities’, ‘Wholesale & Retail Trade, Repair of Vehicles’, and ‘Human Health & Social Work’. Travel to these types of industries would likely be more accessible by car (based on journey time and convenience) followed by and compared to public transport given their location.

The Business Register and Employment Survey (BRES) indicated approximately 125,000 jobs existed in Fife in 2022.

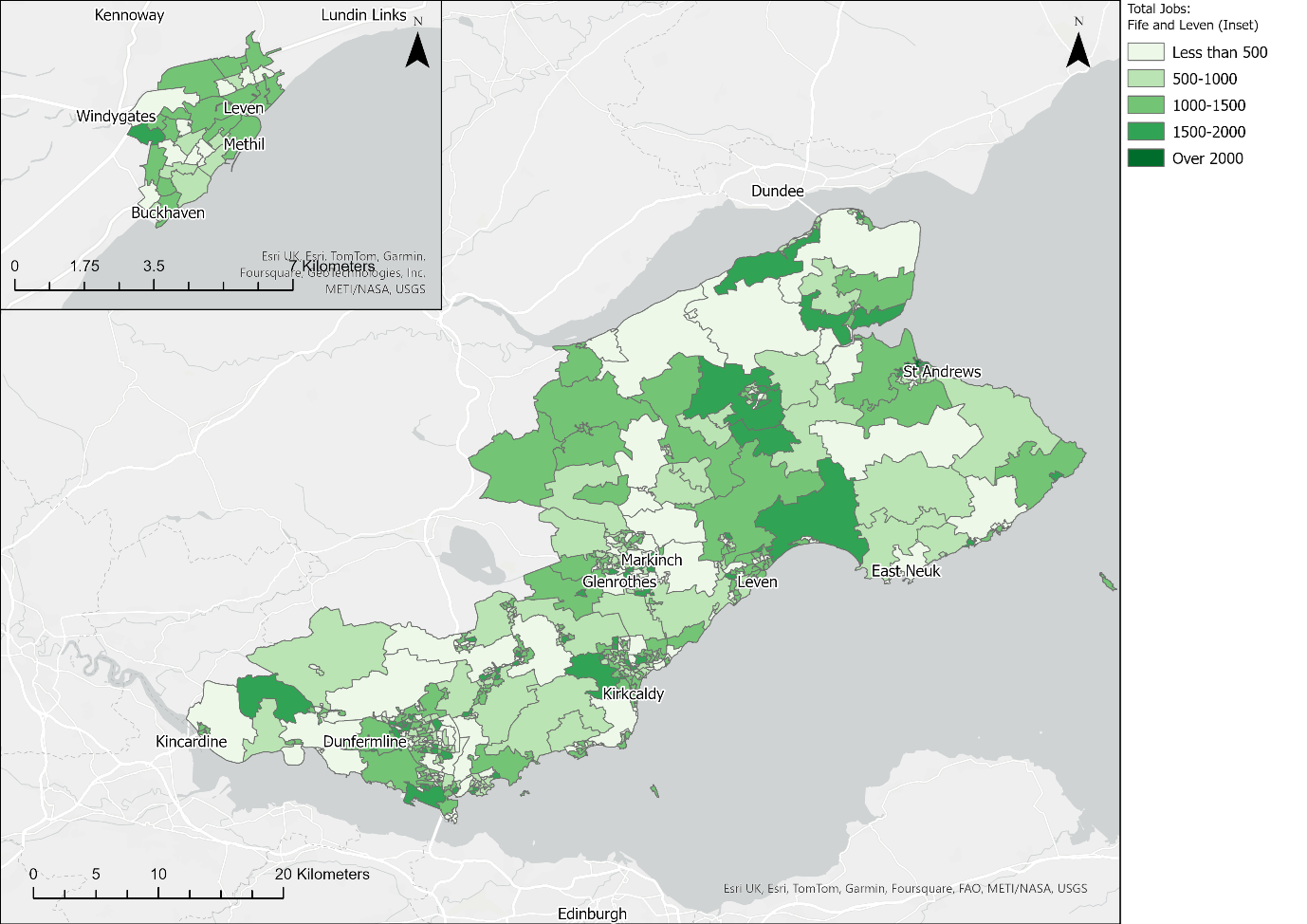

Figure 4‑3 shows the number of jobs per data zone, of which Kirkcaldy can been as a significant location for employment in relation to Levenmouth. Based on trips between Leven Bus Station and Kirkcaldy Bus Station, the journey time is approximately 22 minutes by car whereas the journey time by public transport is longer with a journey time of 32 minutes. It is anticipated that the introduction of the new rail link could reduce the journey time by four minutes from 18 minutes to 14 minutes in total, compared to car and bus, respectively.

Dunfermline also shows a similar number of existing jobs. The current public transport journey time to Dunfermline Bus Station from Leven Bus Station is one hour and 40 minutes. By comparison, car journey time can be between 35 to 55 minutes (based on a Tuesday AM travel time). With the new rail link (based on the 2025 timetable), this is expected to reduce by approximately one hour compared to bus to approximately 40 minutes via the hourly direct service Cowdenbeath and Dunfermline, making it a compelling alternative.

Beyond Fife, the new rail link may improve the connection and ability to travel by public transport to employment opportunities located in major cities that were previously not accessible. This is shown in the journey time modelling and analysis Table 4‑2.

|

City |

Jobs |

Baseline journey time by public transport (hh:mm) |

Anticipated journey time by public transport (bus and rail) post-opening (hh:mm) |

Population catchment by baseline journey time |

||

|

Dunfermline |

27,275 |

01:30 |

00:26 |

0% |

16.8% |

59.1% |

|

Edinburgh |

294,925 |

01:40 |

01:15 |

0% |

3.5% |

42.3% |

|

Glasgow |

381,760 |

02:40 |

1:45 - 2:15 |

0% |

0% |

0% |

|

Dundee |

72,425 |

01:00 |

No change anticipated |

13.3% |

54.7% |

54.7% |

|

Perth |

30,550 |

1:20 to 1:50 |

No change anticipated |

0% |

0% |

59.1% |

|

Stirling |

43,020 |

2:00 to 2:15 |

No change anticipated |

0% |

0% |

0% |

Access to key services

Localities

This analysis presents the existing accessibility by public transport from Levenmouth to a selection of other key localities (populated settlements) within Fife, where key services, jobs and trip attractors are located. Data tables are provided in Appendix C in the accompanying technical appendices.

In summary:

- For the localities within the Levenmouth Area Committee boundary (i.e. Levenmouth plus the Wemyss Villages and Lundin Link), these locations can be accessed by at least 65% of the Levenmouth population within a public transport journey time of 30 minutes. It is anticipated that the Levenmouth Reconnected new/revised local bus services operating and active travel infrastructure in place, in tandem with the Levenmouth Rail Link opening will have a positive impact on population accessibility to localities and key services within the Levenmouth area.

- For localities found in East Neuk, the majority of the Levenmouth population can access Elie and Earlsferry, Pittenweem, St Monans and Anstruther within a 90 minute journey by public transport.

- For localities located on the Fife Circle rail line, the most accessible are Glenrothes, Kirkcaldy and Markinch, whereby between 21% and 37% of the Levenmouth population can access them within a 30 minute public transport journey time. The catchment then increases to over 85% for journey times within 60 minutes. It can be expected that journey times to the localities located on the Fife Circle line would see an improvement with the Levenmouth Rail Link in place, resulting in an increase in the population accessibility catchment by public transport.

- St Andrews and Cupar are the most accessible localities in North Fife from Levenmouth by public transport, with approximately 30% of the Levenmouth population able to access them within a journey time of 30 minutes, increasing to over 75% within a 60 minute public transport journey time. There may be an improvement in journey times to settlements within Levenmouth (such as Methil and Buckhaven) with the Levenmouth Rail Link in place, noting interchange at Kirkcaldy would be required.

Access to healthcare

The healthcare sites considered are those listed on the NHS Fife website – inclusive of A&E, MIU and Community facilities. In addition, Ninewells Hospital in Dundee, Perth Royal Infirmary and the Western General and Royal Infirmary in Edinburgh have been included given their major significance in the Tayside and Lothian/East regions of Scotland for both healthcare and employment. In summary for the Fife-only hospitals (with Appendix C in the accompanying technical appendices providing the full hospital list data tables):

- The most accessible A&E department is the Victoria Hospital in Kirkcaldy, with the majority of the Levenmouth population being able to access it within a 60 minute journey by bus, though only 17% can within 30 minutes. With the Levenmouth Rail Link in place, it is not anticipated to have a meaningful reduction on journey time to the Victoria Hospital from Leven itself due to the requirement to interchange, as Kirkcaldy station is a ten minute bus journey. There already exists a direct bus service between Leven bus station and Victoria Hospital which may remain more attractive compared to the railway. Residents in Methil and Windygates may benefit due to their proximity to Cameron Bridge station and therefore not requiring to interchange in Leven or Glenrothes via bus.

- Regarding Community Hospitals, both Cameron Hospital and Randolph Wemyss Memorial Hospital are the most accessible by public transport for residents of Levenmouth, with over 75% able to access the latter within a 30 minute bus journey, and nearly 90% within 60 minutes for Cameron Bridge Hospital. The Levenmouth Rail Link may reduce the journey times to these locations, however likely more-so for people living outwith the Levenmouth area travelling from the west.

- The modelling indicated that only 13% of the Levenmouth population can access Ninewells Hospital by public transport within a 90 minute journey time, increasing to 31% within a 120 minute journey time. For Perth Royal Infirmary, the modelling indicated it was not possible to make the journey from Levenmouth within a two hour public transport journey time.

- Edinburgh Royal Infirmary and Western General Hospital are not able to be accessed within a public transport journey time of up to two hours. With the Levenmouth Rail Link in place, it is anticipated (depending on connecting bus times in Edinburgh) it could be possible to access the Western General within the two hour journey time; less so for the Edinburgh Royal Infirmary.

Access to education

Population accessibility catchments have been calculated for access from Levenmouth to Levenmouth Academy (High School), Fife College sites (including Levenmouth Campus) and other Further/Higher education establishments located in Central and East Scotland. In summary (with Appendix C in the accompanying technical appendices providing data tables):

- With Levenmouth Academy and Fife College Levenmouth Campus being located on the same site - approximately 50% of the Levenmouth population can access this location within a 15 minute public transport journey, increasing to 85% within 30 minutes.

- Fife College Glenrothes and Kirkcaldy Campuses can only be accessed by approximately 10% of the Levenmouth population within a 30 minute public transport journey; this increases to approximately 80% within a 60 minute journey.

- For universities, St Andrews is the most accessible whereby up to 85% of Levenmouth residents can access it within 60 minutes (albeit this journey post-opening would still be quicker by bus than rail). Only 31% of the Levenmouth population can access Dundee University within a 90 minute public transport journey. It is noted that, based on the modelling, the University of Edinburgh and Heriot Watt campuses cannot be accessed within a two-hour public transport journey time from Levenmouth.

Status of the local economy in Levenmouth

This section provides both an area profile in terms of the local economy of Levenmouth, as well as results from the Business and Organisation Survey undertaken for this baseline.

Unless stated otherwise, the data in this section is reported at the Levenmouth boundary level, i.e. the immediate populated urbanised settlements of Leven, Methil, Buckhaven, Windygates and Kennoway.

Economic landscape

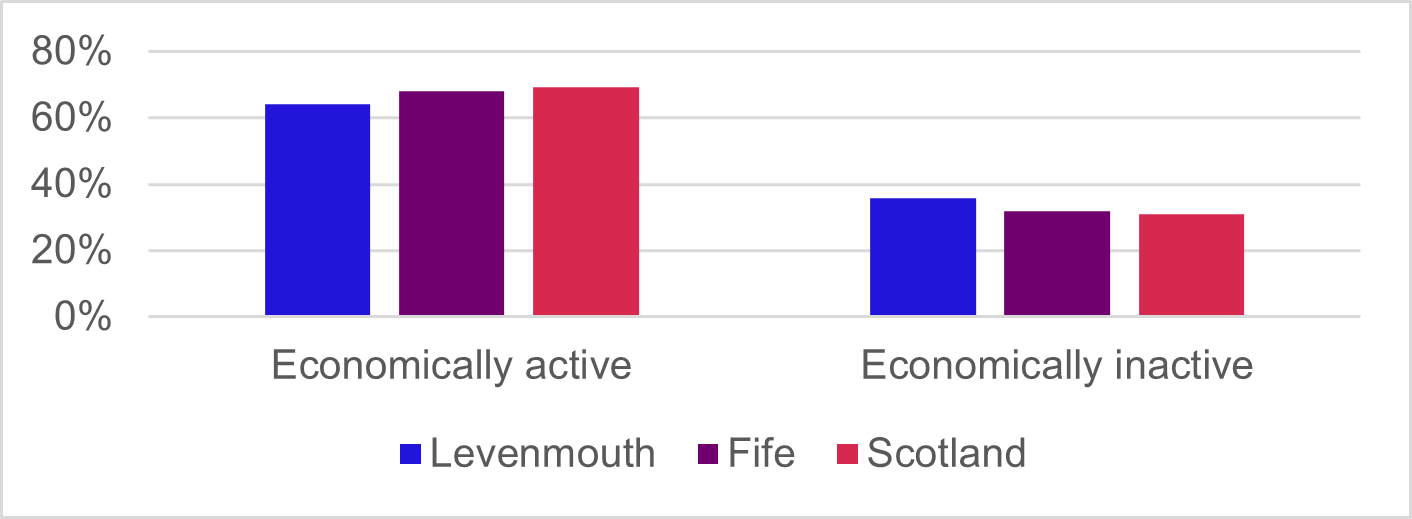

Economic activity within Levenmouth is reported as being lower when compared to both Fife and the rest of Scotland. This is shown in Chart 4‑8 which represents the percentage of the population who are economically active and inactive. Note the economically active category includes people who work part time or full time, self-employed, students and unemployed (seeking employment opportunities).

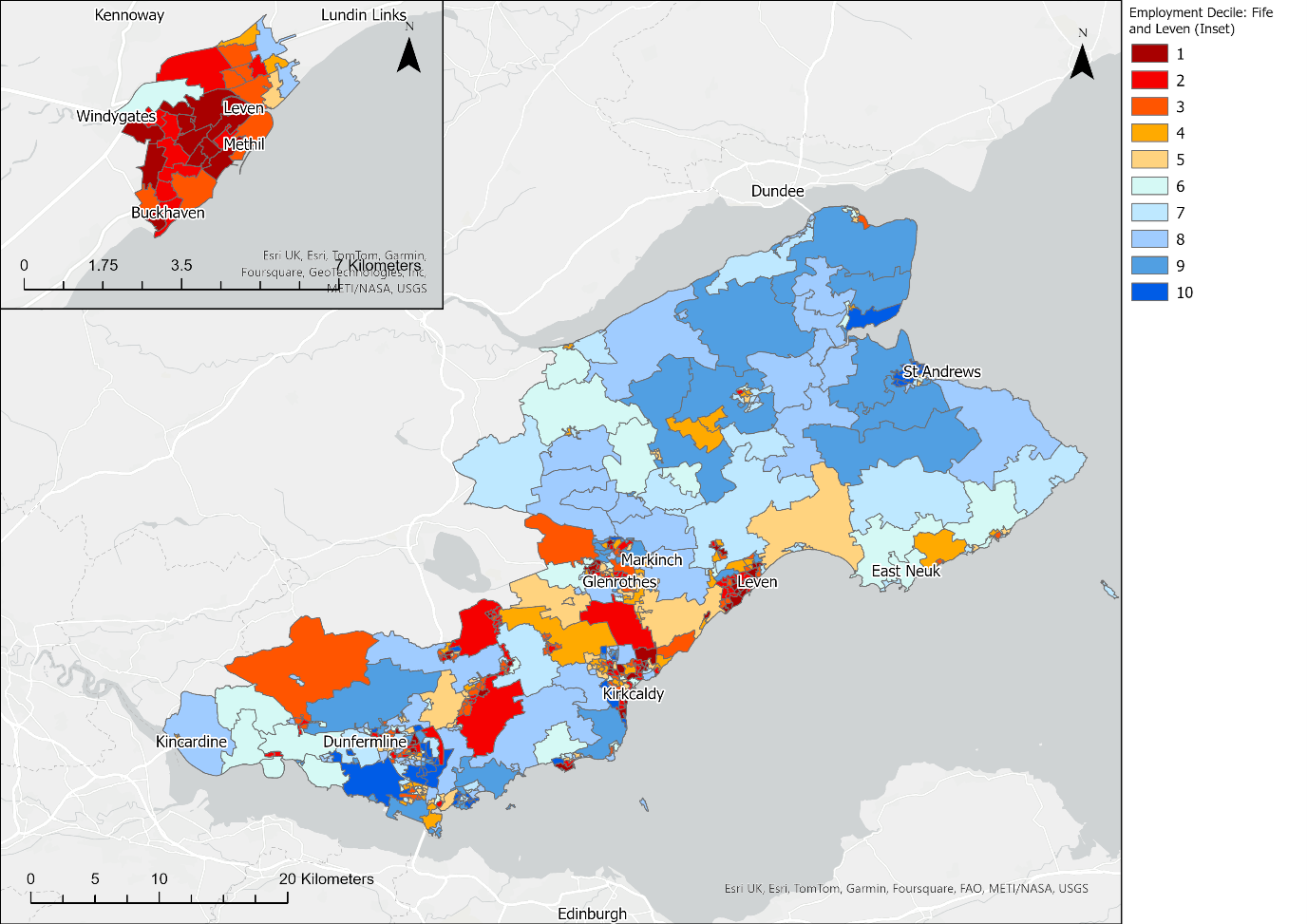

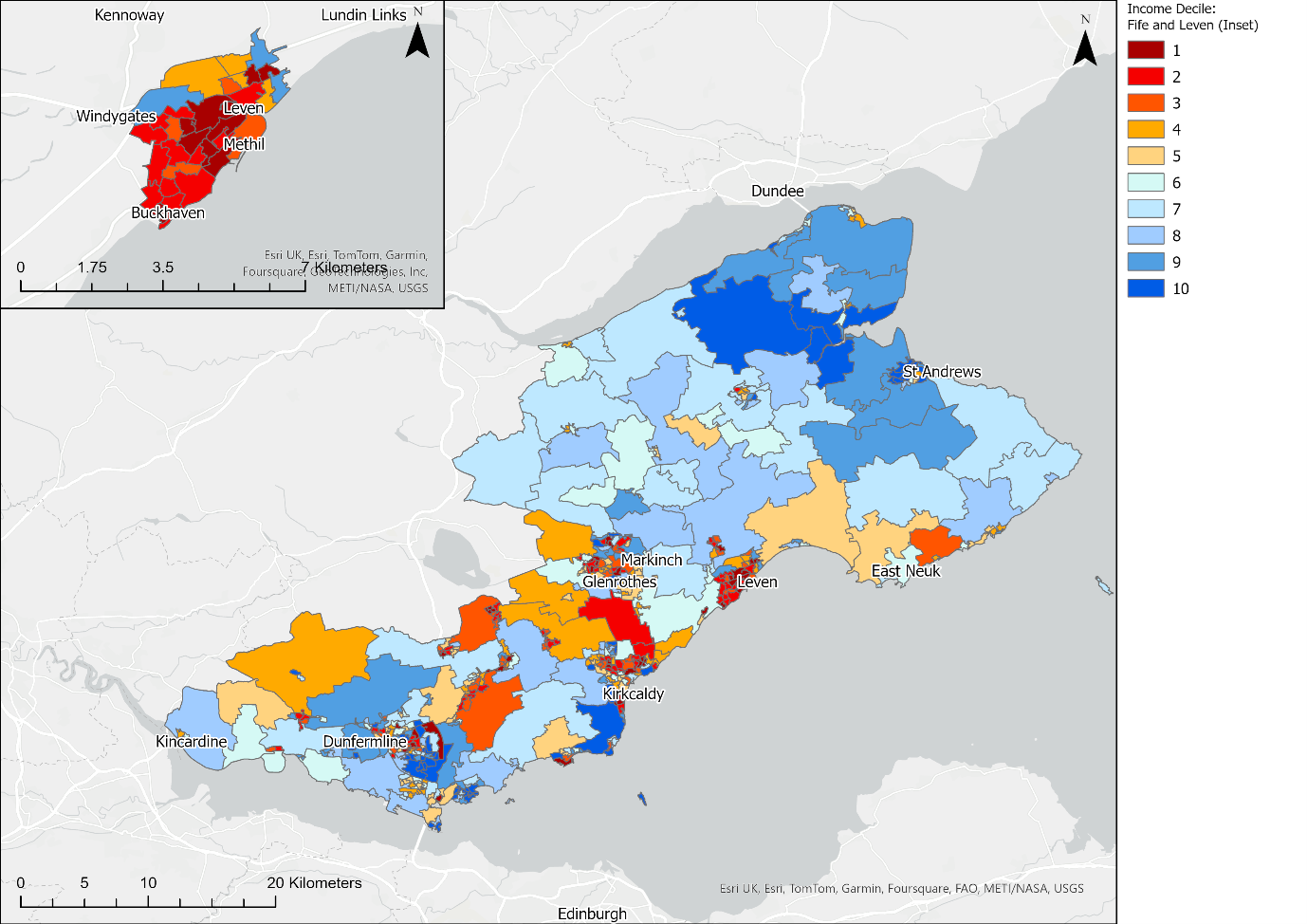

This is further reflected in SIMD, which shows Levenmouth to have relatively high levels of employment deprivation. The employment domain in SIMD takes into account the number of people on job seekers allowance and other unemployment related benefits. Levenmouth shows high levels of employment deprivation, with 49% of the population found within the 20% most deprived nationally, particularly when compared to Fife where 20% of the population is identified as living in areas high employment deprivation (difference of 29 percentage points). Employment deprivation is visible across all parts of the settlement area, including Leven, Methil and Buckhaven, as shown in Figure 4‑4.

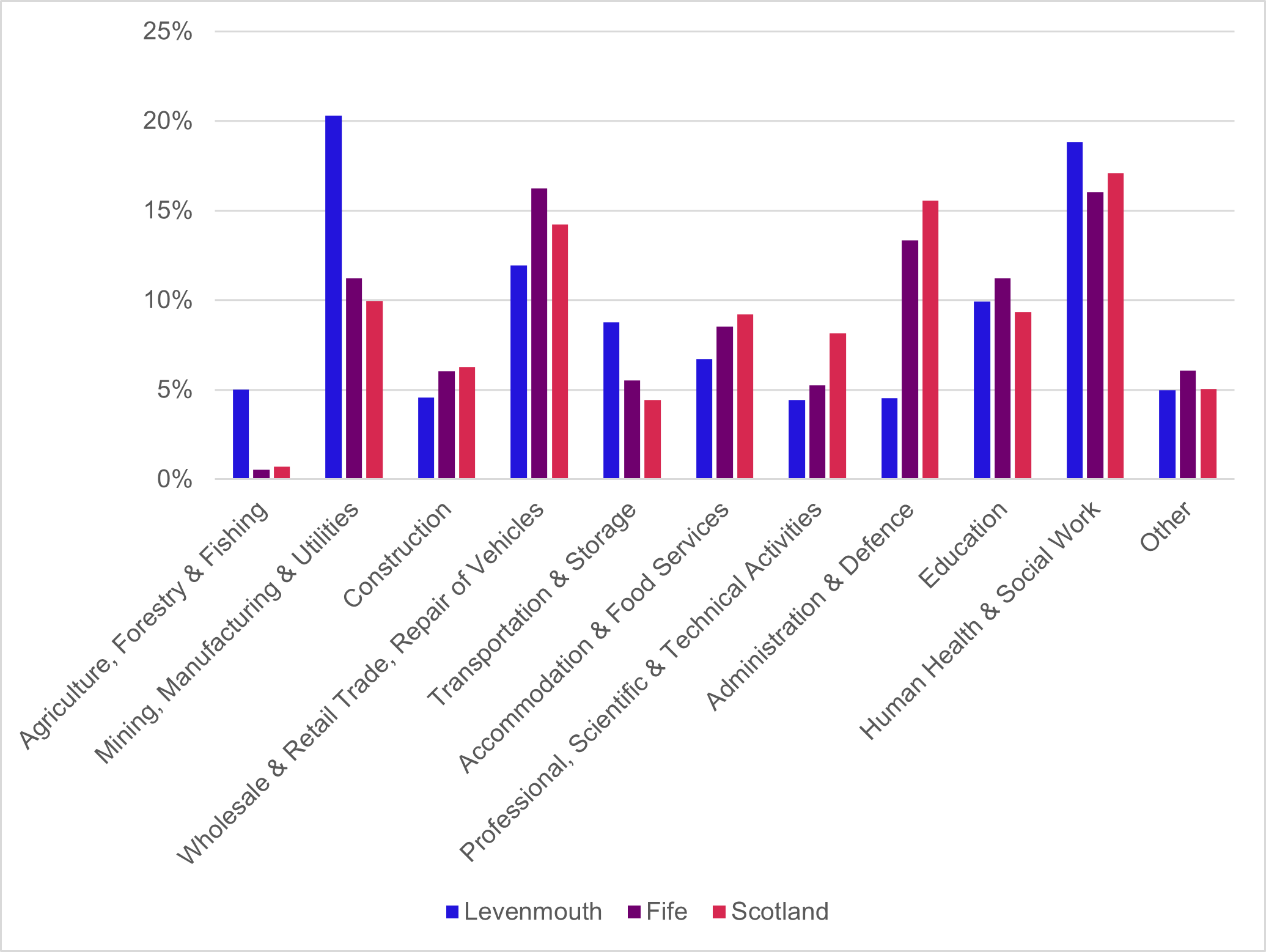

However, Levenmouth does have a number of opportunities located within it that will attract employment related trips locally and trips from outside of the area, though more likely to be from Fife. Business Register and Employee Survey (BRES) 2022 reports that there are over 9,000 jobs located within the Levenmouth area. Over half of the total jobs within the area are comprised of; ‘Mining, Manufacturing & Utilities’ (20%), ‘Wholesale & Retail Trade, Repair of Vehicles’ (12%), and ‘Human Health & Social Work’ (19%). Chart 4‑9 shows the proportional split of jobs across different employment industry categories.

People residing in Levenmouth area are considered to live in income deprived areas relative to the rest of Scotland, accordingly to SIMD – where this domain takes into account income-related benefits such as income support or tax credits. SIMD reports that 49% of the population within Levenmouth is found within the 20% most deprived areas in Scotland, compared to 20% of the population in Fife (difference of 29 percentage points). Most areas within the settlement are considered income deprived, including Leven, Methil and Buckhaven, with the exception of some areas found to the north (as shown in Figure 4‑5).

Levenmouth could be categorised to be an economically disadvantaged area relative to the rest of Scotland. Up to 52% of data zones within Levenmouth fall within the 20% most deprived for income in Scotland which equates to 49% of the Levenmouth population. Compared with Fife which can be seen in Figure 4‑5 to be broadly more affluent than Levenmouth itself. Up to 20% of data zones in Fife (and 20% of the population) live within the 20% most deprived data zones for income.

Attitudes to neighbourhood

All residents were asked about attitudes to their local neighbourhood in the resident survey. The rationale for this question is to determine the attractiveness of Levenmouth as a place to live based on local perceptions, and in the post-scheme implementation evaluation, if the rail link has changed the attractiveness of the area as a place to live.

The majority (98%) of Levenmouth respondents consider their neighbourhood to be a good place to live with 71% considering it to be a very good place to live and 27% a fairly good place to live. Results by area of note include:

- In comparison to the survey area as a whole where at least 68% residents consider their neighbourhood to be a very good place to live, only 42% of Kennoway residents consider the same (however 55% of them consider it a fairly good place to live).

- As many as 28% of Cupar residents indicates they feel poorly about their neighbourhood being a good place to live.

Two thirds (66%) of all resident survey respondents ‘feel very strongly’ about their neighbourhood, with 31% saying they ‘feel fairly strongly’ about their neighbourhood. Up to 80% and 77% of Buckhaven and Leven residents, respectively, feel very strongly about their neighbourhood. Conversely, as many as 10% of Kennoway residents did not overall feel strongly about their neighbourhood.

Business and organisation survey analysis

The sample frame for the survey was comprised from a combination of a bought-in, General Data Protection Regulation (GDPR) compliant database of 654 business contacts within the Levenmouth Area Committee boundary (Electoral Wards 21 and 22) (as shown in Figure 2‑2) and an additional set of 113 contacts in those postcodes identified from a comprehensive web search.

A total of 148 responses were secured, of which 48 were online and 100 by telephone. Of these, 124 were from private sector respondents, nine from public sector respondents and 15 from third sector respondents.

Private sector respondents included the following sectors: retail (35%), accommodation and food service (17%), arts, entertainment, and recreation (10%), manufacturing (9%), human health and social work activities (7%) and construction 6%).

Public sector respondents included education (56%), local government (33%) and sports and leisure (11%). Third sector respondents included national charities (57%), voluntary/community organisations (57%), social enterprises (29%) and an international charity (7%).

Private sector

Length of time operating in Levenmouth

Respondents were asked, thinking about their Levenmouth location, how long their business had been operating at this location. The majority of businesses (74%) had been operating at this location for more than ten years, with a further 12% having been operating at the location for between six and ten years.

Those businesses that had been operating at this location for ten years or fewer were asked to describe the situation with respect to the establishment of their business site at Levenmouth. In 89% of cases, their Levenmouth site had been established as a new business at this location, in 4% of cases it was set up as part of a business expansion and in 7% of cases was a relocation from elsewhere.

Those businesses that had been established for fewer than ten years (and therefore potentially influenced by public announcements of the planned reopening of the Levenmouth Rail Link) were asked as to whether the announcement of the reopening of the rail link had been a factor in their decision to begin operating in the area. In the great majority of cases (85%) this had not been a factor. Two businesses indicated that the announcement of the reopening of rail link had been a major factor in locating their business in Levenmouth.

Advantages/disadvantages to operating in the area

Businesses were given a list of potential advantages and disadvantages for businesses of being located in Levenmouth and were asked to consider whether they considered each of these things to be an advantage, a disadvantage or neither, relative to their competition.

The most common advantages that private sector respondents identified in relation to their Levenmouth location currently were: road links to the site (61%), proximity to customer markets (60%), public transport links to the site (60%) and the quality of the local area generally (60%).

The most common disadvantages that private sector respondents identified in relation to their Levenmouth location currently were: quality of the local area generally (18%), road links to the site (11%) and public transport links to the site (11%).

Recruitment of staff

A notable minority of businesses say they find it difficult or very difficult to recruit staff for their Levenmouth operations (37%). Only 32% described it as being either “very easy” or “easy” to recruit staff, with 31% giving a neutral “neither easy nor difficult” response.

For the majority of businesses, staff levels have remained stable over the last three years (67%), but employment levels have decreased in 21% of cases and increased in only 12% of businesses over this period.

In terms of apprenticeships, 17 (approximately 15%) of Levenmouth businesses who responded indicated they offer apprenticeships (base number 111) The most common barriers to people accessing these apprenticeships are perceived as availability of public transport (59%) and cost of public transport (44%).

All respondents were asked how they would describe the impact of current provision of public transport in the area on the recruitment of staff. Almost a third (31%) considered that current public transport provision limited recruitment (including 9% that suggested this strongly limited recruitment). This compared to a smaller number (9%) that considered public transport helped recruitment, (of this group a further 3% suggested this strongly helped recruitment. The most common response was, however, that current provision of public transport neither limited nor helped recruitment (60% of respondents).

Where public transport was seen as limiting recruitment, this was most commonly due to the availability of services (65%), to accessibility of train station/bus stop/bus (59%) and to frequency (44%). When it was seen as helping recruitment, this was most commonly in relation to accessibility of train station/bus stop/bus (70%), to distance to train station/bus stop (50%), reliability (40%), overall journey time (40%) and to availability of services (40%).

Markets served and suppliers

Respondents were then asked how they would describe the impact of the current provision of public transport in the area on customer footfall. Note – there was a slightly lower base number of respondents (107) reflecting that the “footfall” concept was not relevant to some businesses.

The results suggest that a proportion of respondents considered that current public transport provision limited footfall (33% overall including 10% that suggested this strongly limited footfall). This compared to 17% of respondents who considered that current public transport provision helped footfall of whom 7% suggested this strongly helped footfall. The most common response was, however, that current provision of public transport neither limited nor helped footfall (49% of respondents).

Where public transport was seen as limiting footfall, this was most commonly due to the accessibility of train station/bus stop/bus (65%) and to the availability of services (58%). When it was seen as helping footfall, this was also most commonly in relation to accessibility of train station/bus stop/bus (72%) and to availability of services (67%).

Private sector businesses serve a wide variety of geographical areas including local Levenmouth (86%) and elsewhere in Fife (65%) markets as well as customers from Edinburgh (35%), elsewhere in Scotland (45%), elsewhere in the UK (25%) and overseas (18%).

Investment

Respondents were asked how the level of “investment in the business” had changed compared to the previous financial year. It was noted that “this could include capital investment or investment in people with the aim of growing or developing the business”. The most common response was that this had not changed (60%). However, respondents were somewhat more likely to say that investment had increased (27% overall, of which 17% increased slightly and 10% increased significantly) as opposed to saying that investment had decreased (13% overall, of which 4% decreased slightly and 9% decreased significantly).

Overall, 22% of respondents indicated that the forthcoming opening of the Levenmouth Rail Link had an impact, with 15% describing this as a slight impact and 7% as a significant impact.

Awareness of the Levenmouth Rail Link reopening

Respondents were asked whether they were aware of the scheduled reopening of the Levenmouth Rail Link before receiving notification of this survey. Almost all private sector respondents were aware of the scheduled reopening of the Levenmouth Rail Link (98%), 2% were not aware.

Anticipated impact of Levenmouth Rail Link

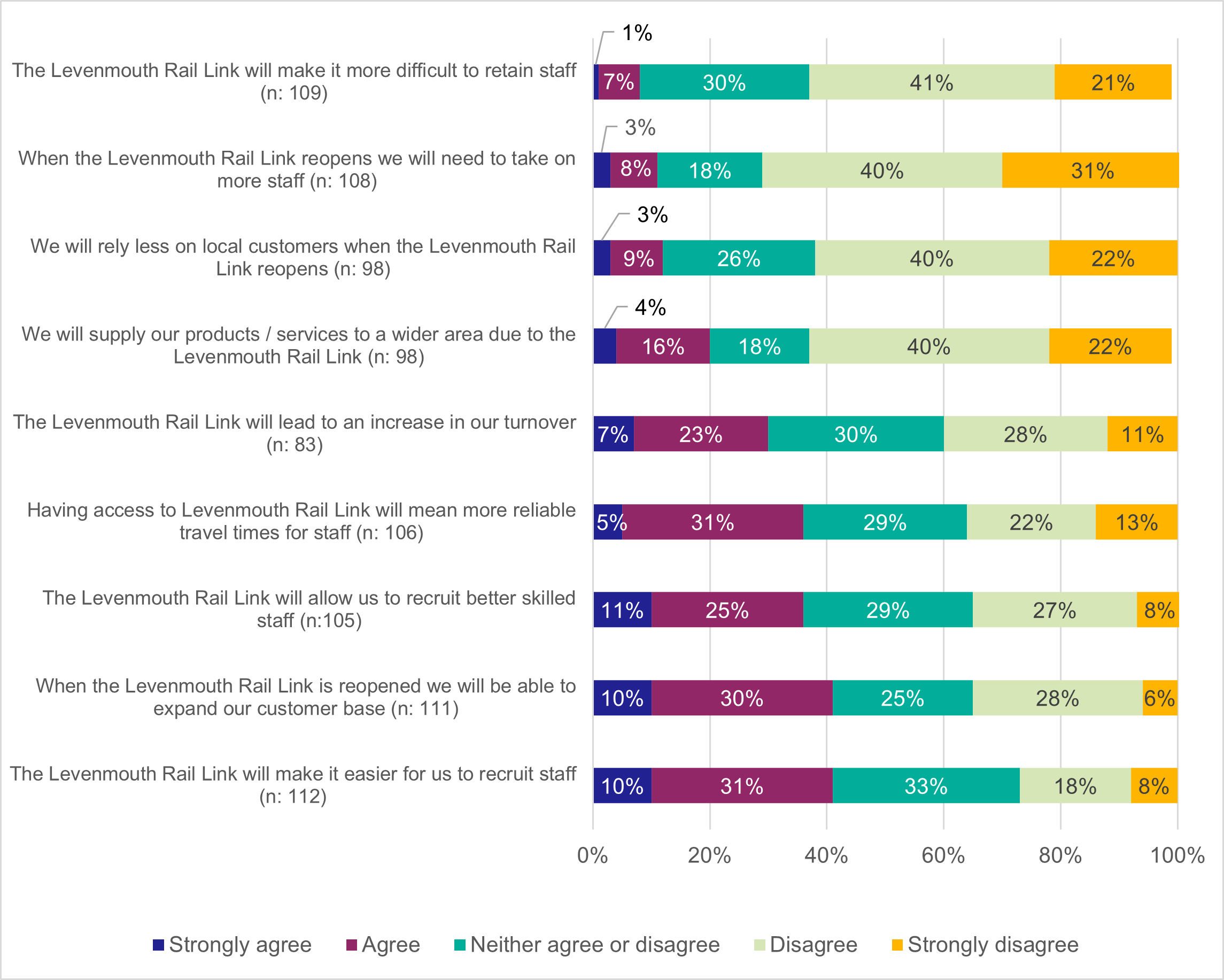

Respondents were asked about the extent of their agreement or disagreement with a number of statements regarding the impact that the reopening of the Levenmouth Rail Link may have on their business. These results are detailed in Chart 4‑10 (it should be noted that ‘Don’t know/Can’t say” responses have been excluded). Results are ordered according to overall agreement.

Private sector respondents were most likely to consider that it will make it easier for them to recruit staff (41% overall agreement), that it will enable them to expand their customer base (40% overall agreement), that it will allow them to recruit better skilled staff (36% overall agreement), that it will mean more reliable travel times for staff (36% agreement) and that it will lead to an increase in their turnover (30%).

Public sector

Awareness of the Levenmouth Rail Link reopening

All nine public sector respondents were aware of the scheduled reopening of the Levenmouth Rail Link.

Advantages/disadvantages to operating in the area

Public sector respondents were given a list of potential advantages and disadvantages of them being located in Levenmouth and were asked to consider whether they considered each of these things to be an advantage, a disadvantage or neither.

Public sector respondents were most likely to consider road links to their site (89%), followed by proximity to service users (78%) and the quality of the local area generally to be an advantage (78%).

Recruitment of staff

Public sector respondents were asked how easy or difficult it was for their organisation to recruit for their Levenmouth operations. Five organisations indicated they found it ‘very easy’, with one saying it was ‘easy’. Conversely, one organisation found it ‘difficult’ and a further organisation saying it was ‘very difficult’. Amongst all nine public sector respondents, staff levels have remained stable over the last three years.

The current provision of public transport in the Levenmouth area is seen as a limiting factor in the recruitment of staff amongst three public sector respondents.

The current provision of public transport in the Levenmouth area is seen as a limiting factor on service user access amongst three of the public sector respondents.

Areas served

Public sector respondents serve a wide variety of geographical areas including local Levenmouth (all nine respondents) and elsewhere in Fife (two respondents) as well as service users from Edinburgh (two respondents), elsewhere in Scotland (two respondents) and elsewhere in the UK (one respondent).

Anticipated impact of Levenmouth Rail Link reopening

Four public sector respondents agreed that the rail link would allow them to recruit better skilled staff; and five said that it would make it easier for them to recruit staff. Three respondents considered that the rail link will enable them to expand their service user base; and two respondents felt that it will mean more reliable travel times for staff.

Third sector

Awareness of the Levenmouth Rail Link reopening

All third sector respondents (15 respondents) were aware of the scheduled reopening of the Levenmouth Rail Link.

Advantages/disadvantages to operating in the area

The factors that third sector respondents were most likely to consider to be advantages of their current location were proximity to service users/customers (12 respondents) followed by public transport links to their site (11 respondents) and the quality of the local area generally (11 respondents).

Recruitment of staff

Six of the third sector respondents say they find it difficult or very difficult to recruit staff for their Levenmouth operations. Employment levels amongst third sector organisations have remained stable over the last three years for seven respondents, whilst they have increased for five organisations and decreased for three organisations..

The current provision of public transport in the Levenmouth area is seen as a limiting factor in the recruitment of staff amongst for five third sector respondents.

Areas served

Third sector respondents serve users/customers from a wide variety of geographical areas including:

- local Levenmouth (all 15 respondents);

- elsewhere in Fife (nine respondents)

- Edinburgh (four respondents);

- elsewhere in Scotland (six respondents);

- elsewhere in the UK (three respondents); and

- overseas (three respondents).

The current provision of public transport in the Levenmouth area is seen as a limiting factor on service user/customer access amongst five of the third sector respondents.

Anticipated impact of Levenmouth Rail Link reopening

Nine third sector respondents considered that rail link would allow them to recruit better skilled staff; nine respondents indicated that it would mean more reliable travel times for staff and eight respondents indicated that it would make it easier for them to recruit staff. Five respondents agreed that the rail link will enable them to expand their service user/customer base.

Visitors and tourism

Just over a fifth (22%) of all businesses/organisations surveyed were involved in the visitor/tourism sector. Of these, 85% were private sector businesses, 6% were public sector organisations and 9% were third sector organisations.

Amongst businesses/organisations involved in the visitor/tourism sector, the estimated average figures for visitors by area or origin indicates 37% being from Fife, 33% from the rest of Scotland, 18% from the rest of the UK and 13% being international.

Respondents in this sector also estimate that 30% of visitors are day trippers, followed by visitors staying on average two days (20%), three to four days (23%), five to seven days (23%) or eight days or more (3%).

Those respondents involved in the visitor/tourism sector were asked to describe in their own words what attracted visitors/tourists to Levenmouth. Comments mainly reflected “golf”, “beaches” and “coastal paths”.

All respondents were aware of visitors using a car/van to travel to the Levenmouth area, followed by 52% being aware of visitors using an “ordinary service” bus and 39% being aware of visitors travelling by coach.

Intentions to use the Levenmouth Rail Link

Awareness of and intention to use the Levenmouth Rail Link

Respondents in both the resident and business surveys were asked about their intentions to use the Levenmouth Rail Link. They were asked specifically for travel to/from Levenmouth, as well as between Cameron Bridge and Leven railway stations.

The majority (93%) of all resident survey respondents overall were aware of the scheduled reopening of the Levenmouth Rail Link. Awareness was slightly lower among younger age groups, specifically residents aged 16 to 21 (85%) and 22 to 34 (88%). Residents are also less likely to be aware in areas such as Cupar (67%), Kirkcaldy (74%) and Glenrothes, Markinch and Thornton (85%). Conversely, residents from Levenmouth itself were much more likely to be aware (99%).

Intention to use the Rail Link between Cameron Bridge and Leven Railway Stations

Just over two thirds (69%) of Levenmouth residents say they anticipate using the Levenmouth Rail Link to travel between Leven and Cameron Bridge railway stations specifically during its first 12 months of operation.

Within Levenmouth, the majority of residents from Methil (90%) anticipate using the rail link to travel between Leven and Cameron Bridge within the first 12 months of operation. This is followed by 73% of Kennoway residents, then 69% of Leven residents. Conversely, at least 83% of Glenrothes, Kirkcaldy and Cupar residents do not anticipate using the Rail Link for this purpose within the first 12 months of operation.

The majority of Levenmouth residents that anticipate using the rail link between Leven and Cameron Bridge intend to use it for leisure purposes (84%), followed to a lesser extent by shopping (56%). A notable proportion of residents intend to use the rail link to connect to onward public transport (25%) or for employment (13%). Less than 5% of residents in each case intend to use the rail link for other purposes.

Intention to use the Levenmouth Rail Link to travel to/from Levenmouth

Over a half (56%) of residents say they anticipate using the Levenmouth Rail Link to travel to and from the Levenmouth area during its first 12 months of its operation, with as many as 71% from Levenmouth indicating they would use it. Within Levenmouth, as many as 93% of Methil residents, followed by 74% of Kennoway and 70% of Leven residents indicate they will use it to travel to/from Levenmouth within the first 12 months of operation.

The majority of Levenmouth residents that anticipate using the rail link to travel to and from the Levenmouth area, intend to use it for leisure purposes (86%), followed to a lesser extent by shopping (56%) and visiting friends or relatives (55%). A notable proportion of residents intend to use the rail link to connect to onward public transport (30%) or for employment (17%). Up to 6% or less of residents in each case intend to use the rail link for other purposes.

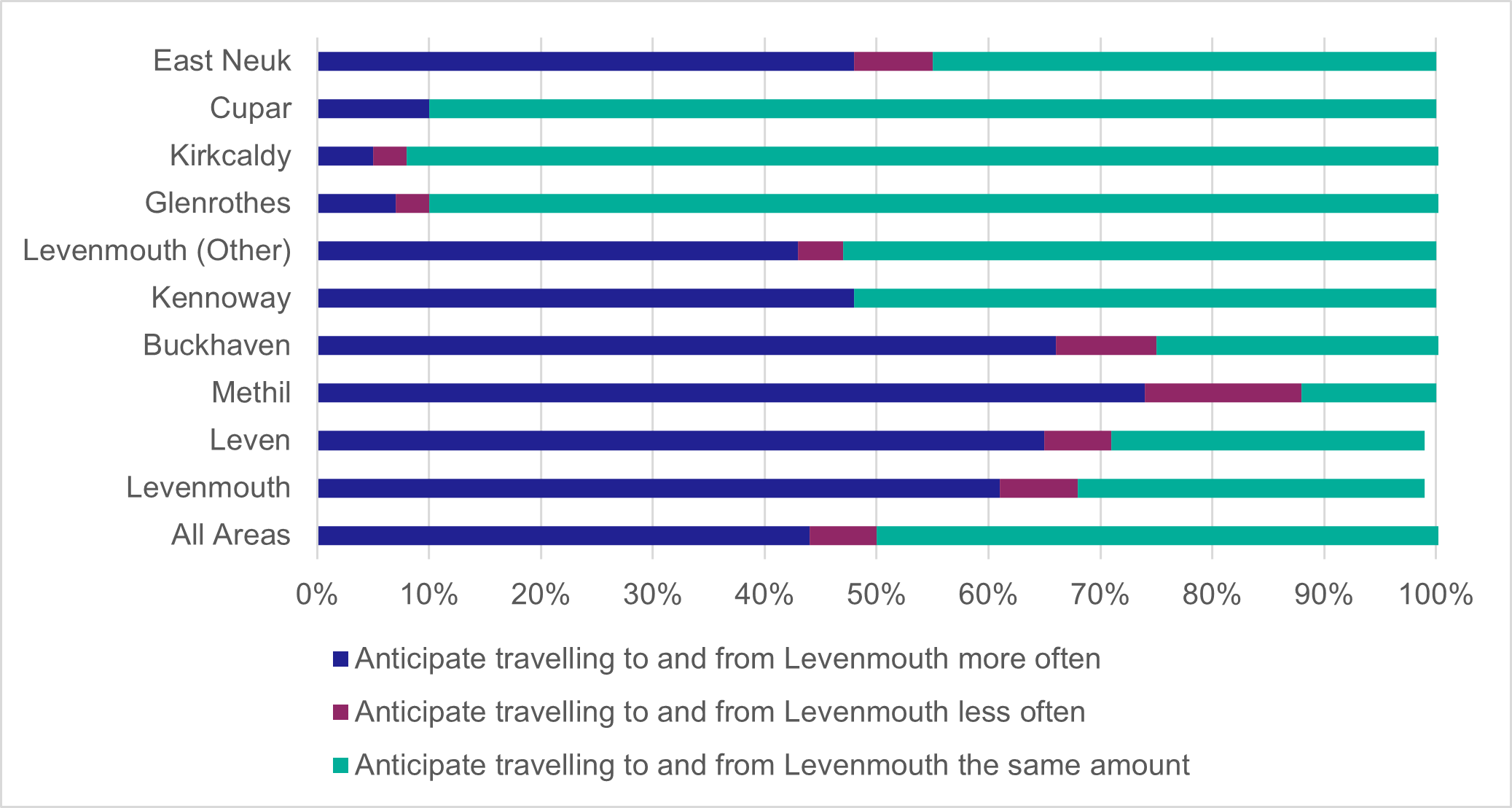

Impact of the Levenmouth Rail Link on travel demand within, to and from Levenmouth

All respondents, regardless of whether or not they anticipated using the Levenmouth Rail Link, were asked to indicate how it will impact how often they travel to and from Levenmouth.

Just over half of residents say they anticipate travelling to and from Levenmouth about the same amount, after the rail link reopens (52%) while just over two-fifths (44%) anticipate travelling more often. Comparatively few anticipate travelling to and from Levenmouth less often (6%). Among those that say they anticipate using the rail link, 74% anticipate travelling to and from Levenmouth more often.

The survey results indicate:

- Methil has the greatest percentage of residents (74%) who anticipate travelling more often to/from Levenmouth; whilst only 48% of Kennoway and 43% of other Levenmouth area residents anticipate travelling to/from Levenmouth more often as a result of the rail link.

- Two thirds (66% and 65%) of Buckhaven and Leven residents, respectively, anticipate travelling to/from Levenmouth more following the reopening of the Levenmouth Rail Link.

- Almost half of East Neuk residents anticipate travelling to/from Levenmouth as a result of the Levenmouth Rail Link;