Battery Electric Vehicles

This section explores the key findings for Battery Electric HGV Vehicles (BEVs), assuming all HGV fleets to be electric. There is no clear evidence on future intentions of fleets which would enable an alternative ratio to be used. It gives a suggested network of en route charging locations, and describes the viability of the routes given in the data under three scenarios:

- Home depot charging only.

- En route charging only.

- Home depot and en route charging.

The results from each scenario, including any additional stops compared to current diesel HGV journeys, are summarised in Table 1. The best scenario is C, where both depot and en route charging are available – all routes can be completed, although some may require additional stops for charging.

Scenario A, with depot charging only, has 33% of routes incurring a flat battery event with no opportunity to recharge. Of the 65% routes that complete, some violate the 20% minimum battery charge threshold.

Scenario B, with en route charging only, supports almost all routes. Over longer routes, the number of stops does not vary significantly from Scenario C, as vehicles may just charge sooner. However, for shorter routes, 2% remain unable to be completed; and over a larger sample, this can represent a significant number of journeys.

Having both en route and depot charging, as in Scenario C, is the best option for all operations included in the dataset. The locations for non-depot charging infrastructure are discussed on page 8.

In Scenario C, 61% of modelled journeys can be completed without any charging stops while between the depot, destination and return (View Table 1). This occurs without any vehicles violating the 20% minimum battery charge threshold. 12% require one stop en route and 27% require more than one stop. In this scenario, BEVs trucks would only travel an average of 15 km more than the diesel equivalent for charging diversions.

Some remote routes require further analysis. View Future Work.

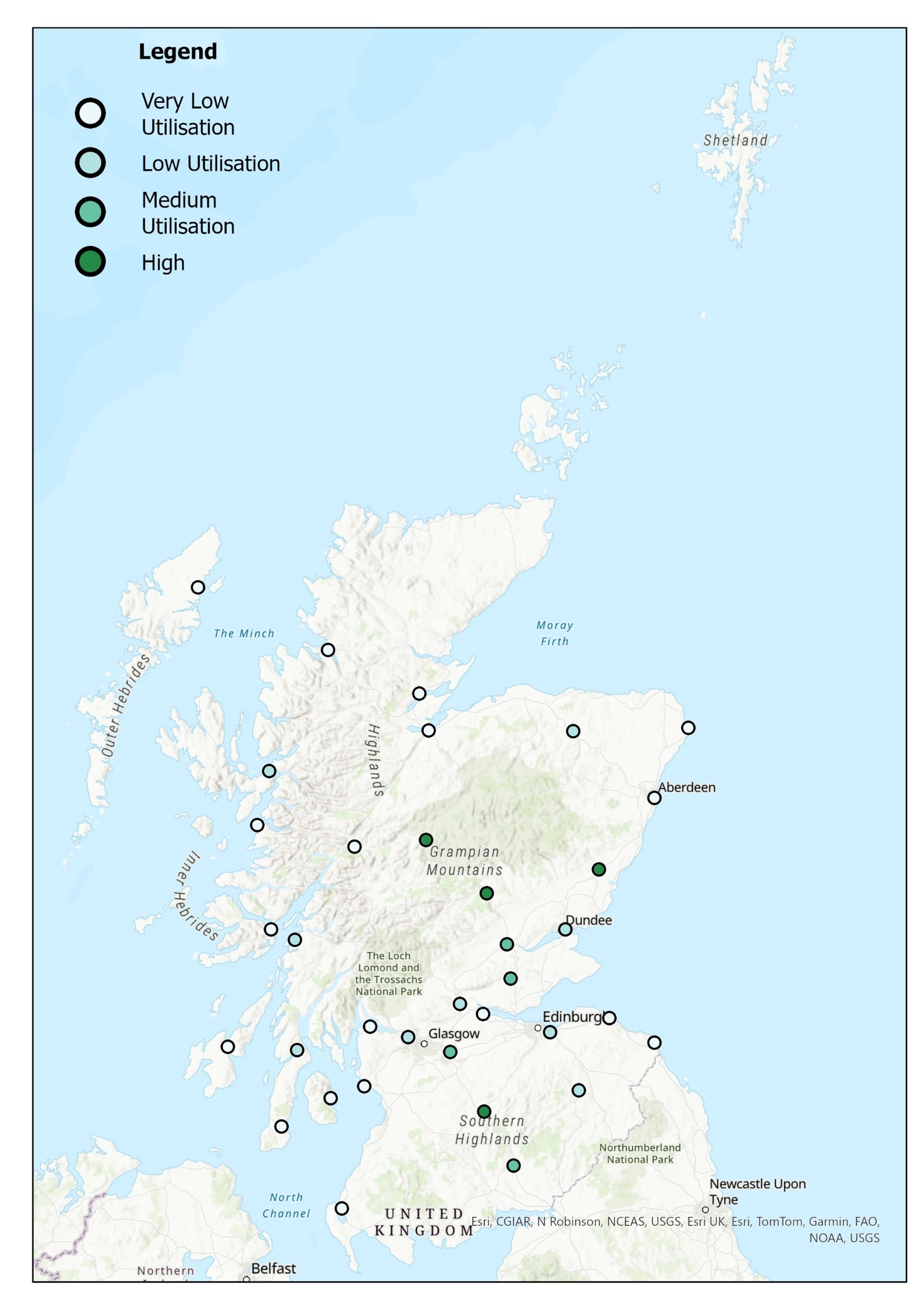

Charging Hot Spots

Analysis of journey data revealed heavy usage of specific routes, particularly along the A9 (Stirling-Perth-Inverness), A90 (Perth-Aberdeen), and M74 (Glasgow-Carlisle) corridors. These critical corridors for freight movement within Scotland would benefit significantly from strategically placed en route charging stationsto support BEV journeys.

The high utilisation hot spots are marked in Figure 3 and outlined in Table 2. The longest distance on the mainland between these potential charging locations is 106km to Cairnryan. The median distance between charge points is 43km. Further investigation to ensure sufficient coverage for remote and critical routes is planned in the future.

| Scenarios | Scenario A (depot charging only) | Scenario B (en route charging only) | Scenario C (both) |

|---|---|---|---|

| % routes unable to complete | 33% | 2% | 0% |

| % complete with no extra stop | 65%* | 59% | 61% |

| % complete with +1 stop | 2% | 12% | 12% |

| % complete with +2-3 stops | 0% | 20% | 20% |

| % complete with 4+ stops | 0% | 7% | 7% |

Real World Trials & Pathway

Switching to BEVs is demonstrated here to be feasible and more than half of journeys can be done without an extra charging stop. As with any model, real-world trials to validate the assumptions and unforeseen challenges regarding vehicle movements are critical. Current and future planned trials consider both the soft (behaviour, opinion) and hard (technology related) challenges with implementing BEVs into existing operations. These trials can also help understand ways to mitigate any impact of additional stops.

Battery electric HGVs are already in use on UK roads and the HGV Decarbonisation Pathway for Scotland states that where the technology is proven and commercially viable, haulage, energy and finance businesses should be transitioning now.

| Location | Number of uses (annual) | Total charge delivered (MWh) |

|---|---|---|

| Dalwhinnie | 11,180 | 2,357 |

| Ballinluig | 8,801 | 1,409 |

| Stracathro | 8,490 | 2,045 |

| Abington | 6,950 | 1,571 |

| Kinross | 4,662 | 945 |

| Annandale Water | 3,835 | 937 |

| Broxden | 3,625 | 822 |

| Mossend | 2,890 | 658 |

| Clydebank | 2,538 | 576 |

| Dundee | 2,152 | 476 |